China's Quiet Dominance in AI-Driven Drug Discovery

For decades, the global pharmaceutical industry regarded China as a capable manufacturer of generic medicines and active pharmaceutical ingredients (APIs) the workshop, not the laboratory. That characterisation is becoming obsolete with striking speed. Driven by coordinated state investment, a sweeping regulatory overhaul, and the emergence of homegrown AI drug-discovery platforms, China has quietly positioned itself at the forefront of one of medicine's most consequential technological shifts.

The evidence is accumulating in research publication counts, clinical trial registrations, out-licensing deal values, and the policy architecture that underwrites it all. What follows is a data-grounded examination of how China built this position and what it means for the global pharmaceutical order.

The Policy Foundation: Planning AI Into the Drug Pipeline

China's ascent in pharmaceutical AI did not happen by accident. It is the product of layered, long-horizon planning stretching from the State Council to provincial pharmaceutical hubs. The 14th Five-Year Plan (2021–2025), administered through the National Development and Reform Commission (NDRC), designated artificial intelligence as one of the country's core "Innovation 2030" strategic priorities, alongside quantum information and integrated circuits. The life sciences sector was a direct beneficiary.

The National Medical Products Administration (NMPA) has operationalised these priorities through successive regulatory reforms. The jointly issued 14th Five-Year Plan for National Drug Safety and High-Quality Development set concrete targets: formulating or revising 2,650 standards for drugs, medical devices, and cosmetics; issuing 480 new guidelines; and fast-tracking innovative drugs with clear clinical value. In March 2025, the State Council's Opinions on Comprehensively Deepening the Reform of Drug and Medical Device Regulation (GBF [2024] No. 53) reinforced these commitments by strengthening standards for next-generation medical technologies explicitly including AI.

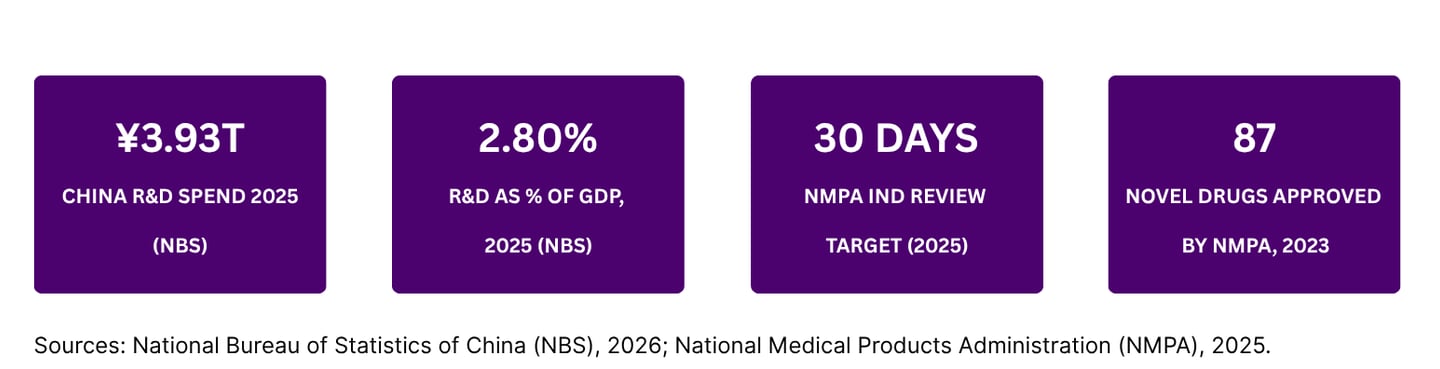

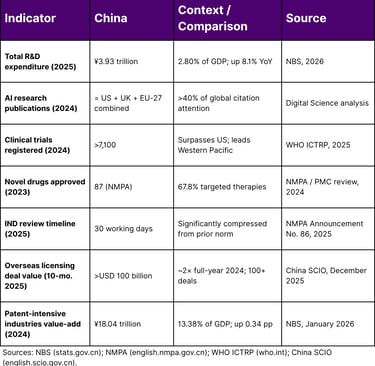

Most significantly for drug discovery timelines, the NMPA announced in October 2025 (Announcement No. 86) that Investigational New Drug (IND) applications for eligible innovative drugs would receive review decisions within 30 working days of acceptance a transformative compression of timelines for AI-designed candidates entering clinical development.

Policy Signal: In November 2024, China's Reference Guide for AI Application Scenarios in the Healthcare Industry identified 84 distinct AI use cases across four healthcare categories, explicitly including drug target identification, virtual screening, and clinical trial design providing formal state endorsement for AI's role throughout the discovery pipeline.

The R&D Investment Surge

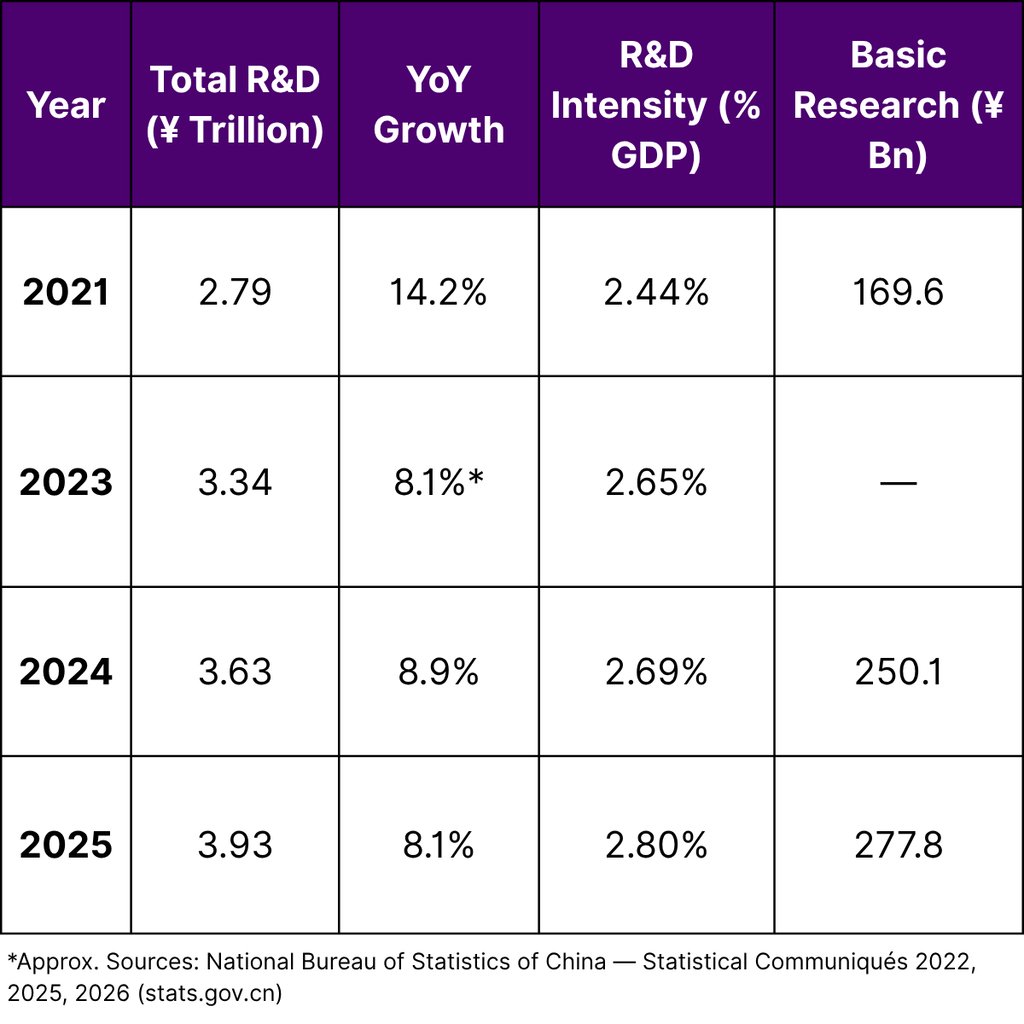

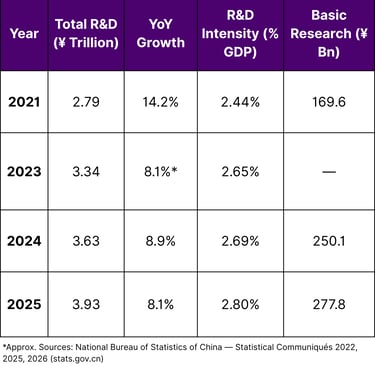

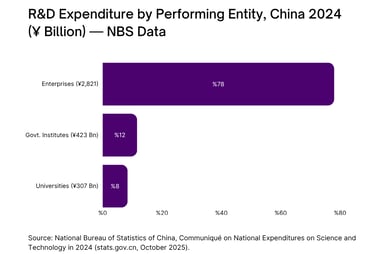

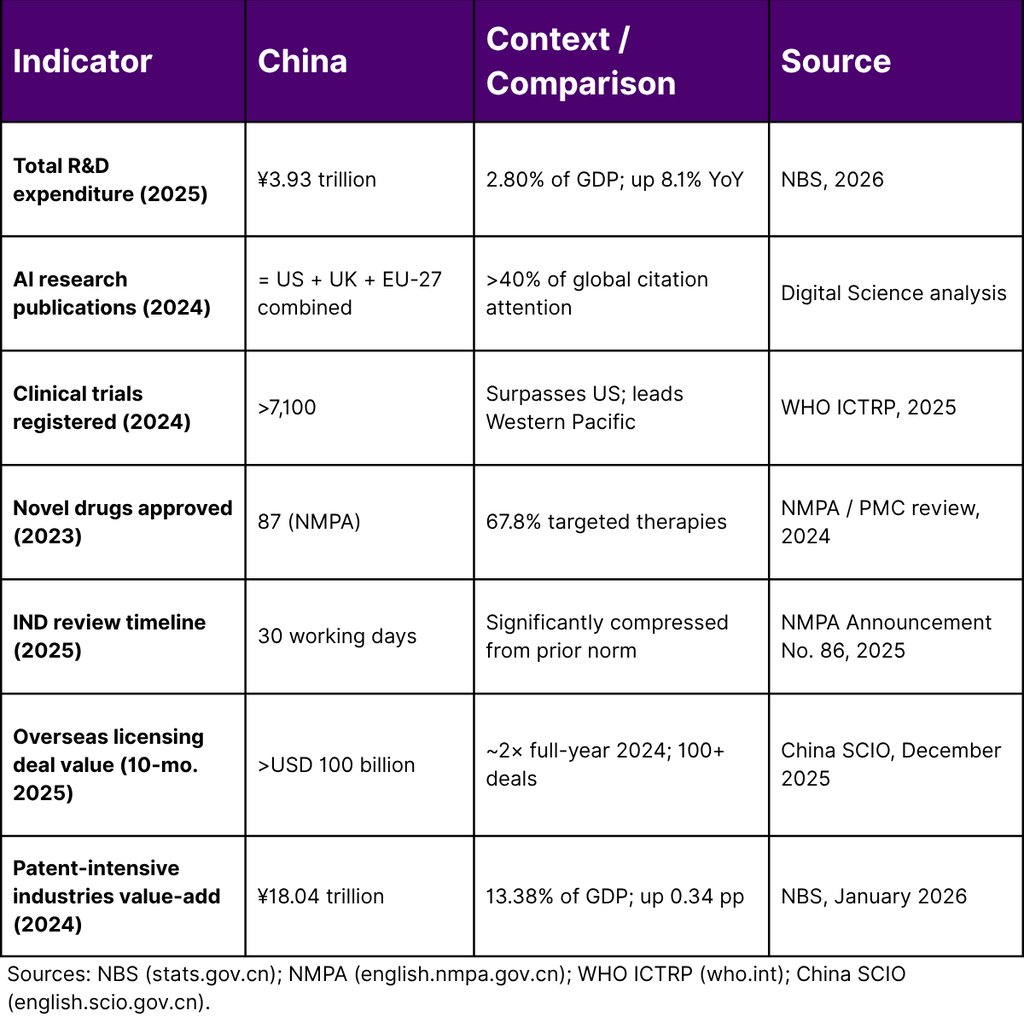

The policy superstructure is backed by national-scale financial commitment. According to the National Bureau of Statistics of China (NBS), total national R&D expenditure reached ¥3,926.2 billion (approximately USD 545 billion) in 2025, an increase of 8.1% over 2024, representing 2.80% of GDP the highest intensity on record. Funding for basic research climbed even faster, rising 11.1% year-on-year to ¥277.8 billion.

The 2024 figure, also released by NBS, recorded ¥3,632.68 billion in total R&D investment, an 8.9% increase over 2023, with applied research expenditure growing at 17.6% the fastest of all R&D categories. High-technology manufacturing the sector encompassing pharmaceutical and biotech firms invested ¥766.89 billion in R&D in 2024 alone, growing 10.2% year-on-year, with R&D intensity reaching 3.35% of business revenue.

Table 1: China National R&D Expenditure Trend (NBS Data)

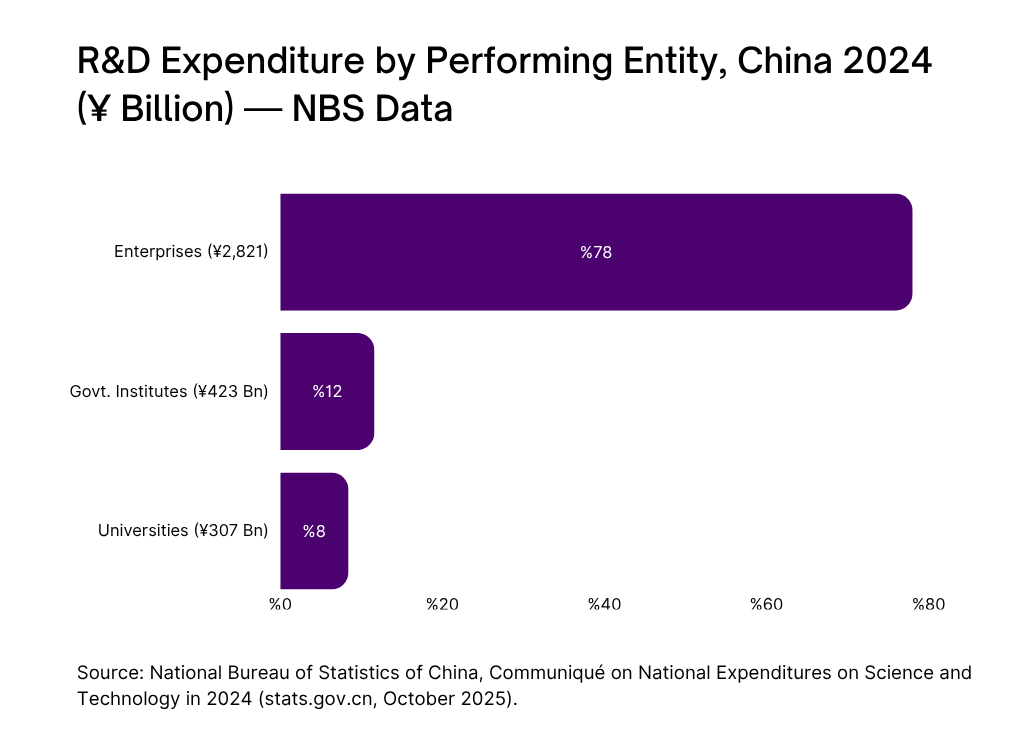

National fiscal expenditure on science and technology reached ¥1,262.92 billion in 2024, a 5.3% increase over 2023, with the central government contributing 33.1% and provincial governments providing the balance reflecting the decentralised nature of China's innovation funding, with biotech hubs in Guangdong, Jiangsu, Beijing, and Shanghai each exceeding ¥200 billion in annual R&D spending.

The Regulatory Transformation: Speed as a Competitive Weapon

Investment alone does not translate to drug discovery leadership. China's real structural advantage has been the pace at which its regulatory architecture has evolved to match scientific ambition with administrative efficiency.

The NMPA has joined the International Conference on Harmonization of Technical Requirements for Pharmaceuticals for Human Use (ICH) and applied for pre-accession to the Pharmaceutical Inspection Cooperation Scheme (PIC/S), bringing its standards into alignment with the US FDA and European Medicines Agency. This harmonisation dramatically reduces the time and cost of seeking simultaneous international registrations a critical capability for AI-designed drugs aimed at global markets.

The practical result is striking. AI drug development is now reported to shorten the discovery-to-clinical-candidate cycle from the traditional range of four to eighteen months in China's most advanced facilities. At SSY Group's facility in Shijiazhuang documented by China's State Council Information Office in December 2025 an AI-powered virtual screening system can identify over 100 novel compounds from a library of 300 million in just over a month. The same task previously required two to three years of conventional screening.

"With intelligent screening, we can identify more than 100 new compounds from a library of 300 million in just over a month. Previously, this would have taken two to three years."

— SSY Group, reported by China SCIO, December 2025

Clinical Trial Leadership

A robust AI discovery engine is only valuable if it can move candidates into human testing efficiently. China has built exactly this capability. According to the World Health Organization's International Clinical Trials Registry Platform (WHO ICTRP), the Western Pacific region driven primarily by China and Japan has held the highest annual trial registration count of any WHO region since 2016, with 27,172 trials registered from the region in 2024 alone.

Within the Western Pacific, China ranks first. In 2024, China listed over 7,100 clinical trials, according to reported data, surpassing the United States and widening a lead that was first established in 2021. This volume is the direct result of an enlarged talent base, improved hospital infrastructure, streamlined NMPA approval pathways, and increasingly AI-assisted trial design that improves protocol efficiency and reduces failure rates.

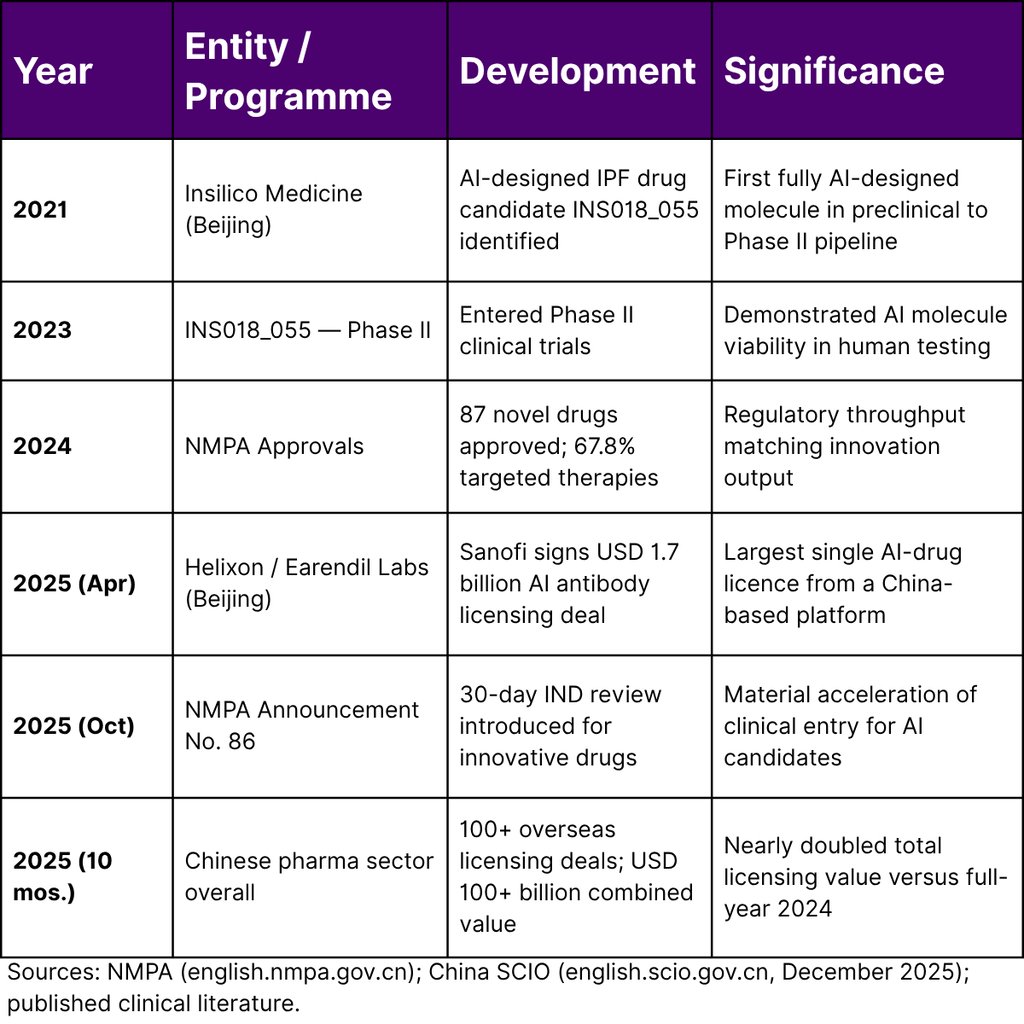

AI Drug Discovery in Practice: Key Milestones

The clearest evidence of China's capabilities is visible in the pipeline. Insilico Medicine, headquartered in Beijing, became one of the first companies globally to advance an entirely AI-discovered small molecule drug INS018_055, targeting idiopathic pulmonary fibrosis into Phase II clinical trials in 2023. The compound was designed using the company's proprietary generative AI platform with no human-guided hypothesis, representing a genuine milestone in autonomous drug design.

The NMPA's own data provides further context on the broader innovation system: in 2023, 87 novel drugs were approved, with targeted drugs the category most amenable to AI-driven design accounting for 67.8% of approvals (59 drugs). The National Medical Products Administration's Centre for Drug Evaluation website now tracks AI-related regulatory submissions as a distinct category.

Table 2: Selected AI-Driven Drug Discovery Milestones China-Based Entities

Structural Advantages and the Data Moat

Beyond capital and policy, China possesses structural advantages in pharmaceutical AI that are difficult for competitors to replicate. Chief among these is the scale and centralisation of health data. With 1.4 billion people and a predominantly public healthcare system, China's medical institutions generate patient datasets of a size and longitudinal depth that few health systems globally can match. This data abundance directly powers the machine learning models that identify therapeutic targets, predict drug-target interactions, and optimise lead compounds.

China also commands significant AI research talent. In 2024, the country's AI research publication output across all domains matched the combined output of the United States, the United Kingdom, and the EU-27, while commanding more than 40% of global citation attention, according to an analysis of AI research trends by Digital Science. The country maintains approximately 30,000 active AI researchers and a large pipeline of postdoctoral talent flowing from science and engineering programmes graduates of which have been growing at double-digit rates, per NBS innovation index data showing a 10.8% annual increase in the proportion of science and engineering graduates.

Table 3: China vs. Global Comparative Indicators in Pharmaceutical AI

The Global Market Context

China's emergence is taking place within a rapidly expanding global market for AI in drug discovery. The global market was valued at approximately USD 6.93 billion in 2025, projected to reach USD 7.62 billion in 2026 and approximately USD 17.81 billion by 2035, growing at a compound annual rate of 9.90%. Within this, the Asia-Pacific region is projected to expand at a notably faster CAGR of 21.1% from 2026 to 2035 nearly double the global average with China as the primary engine.

The most revealing metric of China's maturing position is not domestic market share but deal flow with Western multinational pharmaceuticals. In the first quarter of 2025, Chinese companies accounted for 32% of global biotech licensing deal value up from 21% in both 2023 and 2024 (Jefferies, July 2025 report). This accelerating share reflects the willingness of global pharmaceutical majors including Sanofi, AstraZeneca, and others to licence AI-discovered molecules originating from China-based platforms.

The total value of China's out-licensing deals grew from approximately USD 28 billion in 2022 to approximately USD 46 billion in 2024. In the first ten months of 2025 alone, Chinese pharmaceutical companies signed more than 100 overseas deals with a combined value exceeding USD 100 billion nearly double the total recorded for the entirety of 2024, according to reporting by China's State Council Information Office.

"China has 'structural advantages' in biomedical AI with massive datasets and a large patient pool that few health systems globally can match."

— Scott Moore, University of Pennsylvania, on China's biomedical AI position

Outlook: The "DeepSeek Moment" for Pharma

Many industry observers have begun describing China's pharmaceutical AI trajectory as its "DeepSeek moment" the point at which years of sustained, often quiet investment in research, infrastructure, and regulatory capacity begin to deliver visible, globally competitive breakthroughs. The parallel is apt. Just as DeepSeek's AI models demonstrated that Chinese research organisations could match frontier performance at lower cost, China's AI drug discovery platforms are demonstrating an ability to deliver globally coveted molecules faster and more capital-efficiently than was previously assumed possible.

The Chinese government has signalled continued acceleration. As of August 2025, official statements outlined a target to achieve AI application breakthroughs across key economic sectors by 2027. The pharmaceutical sector explicitly named as a priority in the 14th Five-Year Plan and its successor framework sits at the centre of that ambition.

For global pharmaceutical companies, the implications are twofold. China is simultaneously an increasingly compelling partner for licensing AI-designed molecules, and an increasingly formidable competitor in the race to discover them first. The companies and governments that fail to understand this dual reality and the policy, data, and talent foundations underpinning it risk miscalculating one of the most consequential shifts in the global pharmaceutical industry in a generation.

Frequently Asked Questions

Q1. What has China's government done to specifically support AI in drug discovery?

China has embedded AI drug discovery as a formal priority in the 14th Five-Year Plan (2021–2025). The NMPA has issued specific guidelines for AI in healthcare (including 84 identified use cases in November 2024), compressed IND review timelines to 30 working days for innovative drugs (NMPA Announcement No. 86, October 2025), and the State Council issued comprehensive regulatory reform opinions (GBF [2024] No. 53) explicitly covering AI-enabled drug development. Local governments in pharmaceutical hubs such as Shanghai have further directed funding into AI biotech ventures.

Q2. How much is China investing in R&D overall, and how does this relate to pharmaceuticals?

China's total national R&D expenditure reached ¥3,926.2 billion (approximately USD 545 billion) in 2025, representing 2.80% of GDP the highest intensity on record, per the NBS Statistical Communiqué for 2025. High-technology manufacturing, which includes pharmaceutical and biotech enterprises, invested ¥766.89 billion in R&D in 2024 alone, growing at 10.2% year-on-year.

Q3. What evidence exists that AI is actually accelerating drug discovery in China?

Several concrete examples exist. Insilico Medicine's AI-discovered IPF drug (INS018_055) advanced from AI identification to Phase II clinical trials in a matter of years rather than decades. SSY Group's AI virtual screening system (documented by China's SCIO in December 2025) identifies over 100 compounds from a 300-million-molecule library in about a month a task that previously required two to three years. AI drug development in China's most advanced facilities is now reported to shorten discovery cycles to between four and eighteen months.

Q4. How does China's clinical trial volume compare internationally?

According to WHO ICTRP data (2025), the Western Pacific region led by China has registered the highest number of clinical trials globally per year since 2016, with 27,172 registrations in 2024. Within the region, China ranks first. China registered over 7,100 clinical trials in 2024, surpassing the United States and widening a lead established in 2021.

Q5. What are the key risks or challenges to China's pharmaceutical AI dominance?

While the structural advantages are significant, challenges remain. Geopolitical tensions particularly US-China trade friction create uncertainty around data-sharing, cross-border partnerships, and technology transfer. Regulatory harmonisation, while improving, is not yet fully aligned with all major markets. Additionally, questions around intellectual property protection and data privacy governance continue to influence the confidence of multinational partners. The NMPA and judicial authorities have actively worked to address some of these concerns through updated frameworks during the 14th Five-Year Plan period.

References

National Bureau of Statistics of China. (2026, February 28). Statistical communiqué of the People's Republic of China on the 2025 national economic and social development.

National Bureau of Statistics of China. (2025, October 10). Communiqué on national expenditures on science and technology in 2024.

National Bureau of Statistics of China. (2025, February 7). China's expenditure on research and experimental development (R&D) exceeded 3.6 trillion yuan in 2024.

National Bureau of Statistics of China. (2026, January 8). Announcement on the value-added data of the national patent-intensive industries in 2024.

National Bureau of Statistics of China. (2025, October 30). China's innovation index in 2024.

National Medical Products Administration, People's Republic of China. (2025, October 14). NMPA announcement on optimizing of the review and approval process for clinical trials of innovative drugs ([2025] No. 86).

National Medical Products Administration, People's Republic of China. (2021, December 30). Issuance of the 14th Five-Year Plan for national drug safety and high-quality development.

State Council Information Office, People's Republic of China. (2025, December 29). The new chemistry of 'Made in China'.

State Council Information Office, People's Republic of China. (2025, August 29). China aims for AI application breakthroughs in key sectors in next 2 years, official says.

National Development and Reform Commission, People's Republic of China. (2022). The 14th Five-Year Plan and long-range objectives through 2035.

World Health Organization. (2025). Number of clinical trials by year, country, WHO region and income group (1999–2024).

National Institutes of Health / ClinRegs. (2026, March 9). Clinical research regulation for China.

Zheng, L., Wang, W., & Sun, Q. (2024). Targeted drug approvals in 2023: Breakthroughs by the FDA and NMPA. Signal Transduction and Targeted Therapy, 9(1).

Navigation

© 2026 FyreIgnis Market Research. All rights reserved.

Legal

info@fyreignismarketresearch.com

India