Gene Therapy Gold Rush

The rare diseases treatment market is experiencing unprecedented transformation, projected to reach $374.4 billion by 2030 with an 11.6% CAGR. This explosive growth is driven by revolutionary gene therapy breakthroughs, enhanced regulatory frameworks, and unprecedented investment in orphan drug development. As we stand at the intersection of scientific innovation and commercial opportunity, gene therapy is emerging as the definitive solution for previously untreatable rare diseases, creating one of the most lucrative pharmaceutical market segments of the decade.

Market Landscape: The Rare Disease Renaissance

Market Size and Growth Dynamics

The global rare diseases treatment market represents one of the fastest-growing segments in pharmaceutical history:

2024 Market Value: $195.2 billion

2030 Projected Value: $374.4 billion

Growth Rate: 11.6% CAGR

Investment Surge: 340% increase in gene therapy funding since 2020

Regulatory Environment: The Foundation of Growth

The regulatory landscape has fundamentally transformed to support orphan drug development:

FDA Orphan Drug Act Impact

Since 1983, the Orphan Drug Act has provided crucial incentives:

Tax Credits: 50% credit for clinical testing costs

Market Exclusivity: 7 years of exclusive marketing rights

Fast-Track Review: Accelerated approval pathways

Waived Fees: Reduced regulatory submission costs

European Medicines Agency (EMA) Framework

The EU Orphan Medicinal Products Regulation provides:

10-Year Market Exclusivity: Extended protection period

Protocol Assistance: Scientific advice at reduced fees

Centralized Procedure: Single application across EU

Conditional Marketing Authorization: Early access pathways

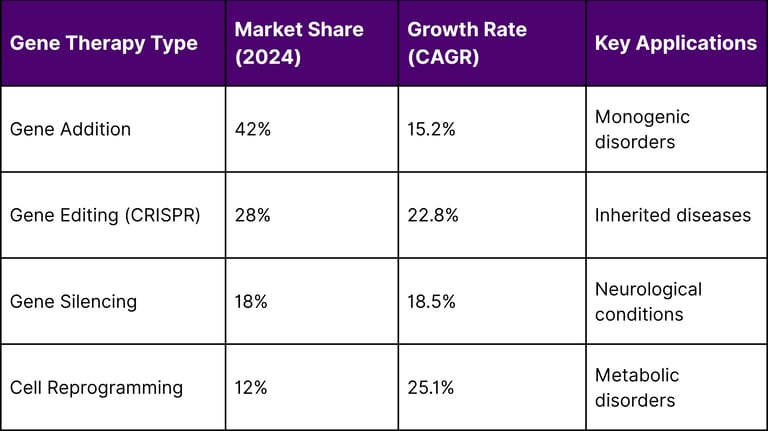

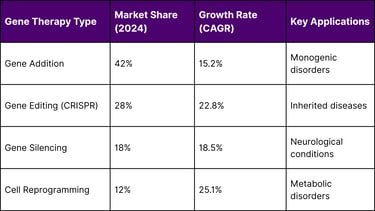

Gene Therapy: The Market Disruptor

Therapeutic Modalities Driving Growth

Note: These CAGR figures represent the expected annual growth rates going forward from the 2024 baseline, typically projected over a 5-10 year period.

FDA-Approved Gene Therapies: Market Leaders

Current Approvals (2020-2025):

Zolgensma (Novartis): SMA treatment, $2.1 million per dose

Luxturna (Spark Therapeutics): Inherited retinal dystrophy

Eteplirsen (Sarepta): Duchenne muscular dystrophy

Spinraza (Biogen): Spinal muscular atrophy

Elevidys (Sarepta): Gene therapy for DMD

Pipeline Analysis: The Next Wave

Late-Stage Development (2025-2027):

180+ gene therapies in Phase II/III trials

45 expected FDA submissions by 2026

$12.8 billion invested in late-stage programs

23 breakthrough therapy designations granted

Disease Area Analysis

Neurological Disorders: The Largest Segment

Market Share: 35% ($68.3 billion by 2030)

Key Conditions:

Spinal Muscular Atrophy: Market leader with 65.7% revenue share

Duchenne Muscular Dystrophy: Fastest-growing at 19.2% CAGR

Huntington's Disease: Emerging gene silencing applications

ALS: Multiple gene therapy approaches in development

Spinal Muscular Atrophy Case Study

Global Spinal Muscular Atrophy (SMA) Treatment Market dynamics:

Current Market Value: $3.2 billion (2024)

Growth Projection: 17.6% CAGR through 2030

Type 1 Dominance: 65.7% of market revenue in 2025

Treatment Paradigm: Shifted from symptomatic to curative approaches

Inherited Metabolic Disorders: High Growth Segment

Market Share: 28% ($104.8 billion by 2030)

Key Therapeutic Areas:

Lysosomal storage disorders

Glycogen storage diseases

Urea cycle disorders

Fatty acid oxidation defects

Hematological Disorders: Innovation Hub

Market Share: 22% ($82.4 billion by 2030)

Leading Applications:

Sickle cell disease gene editing

Beta-thalassemia gene therapy

Primary immunodeficiency treatments

Inherited bleeding disorders

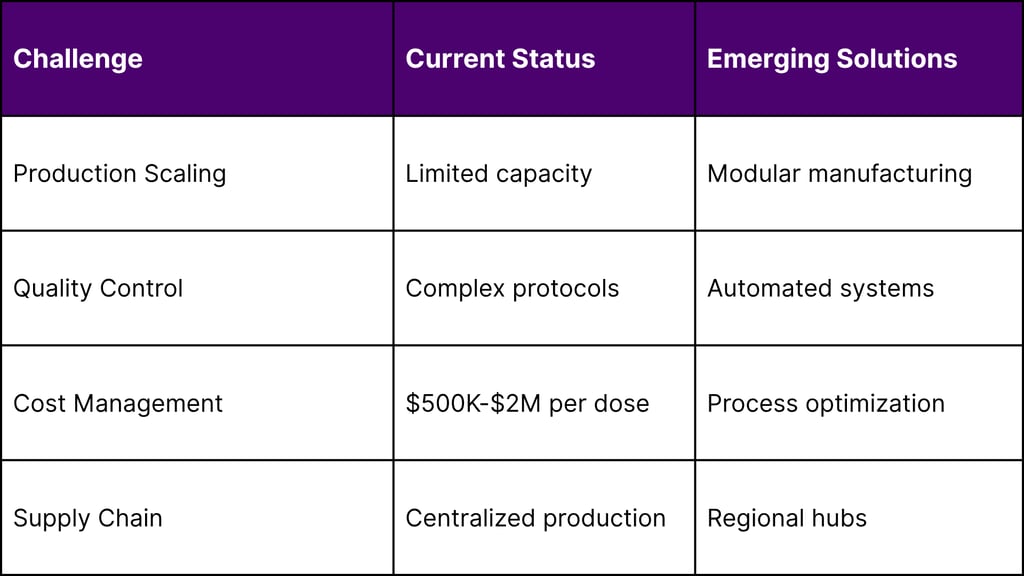

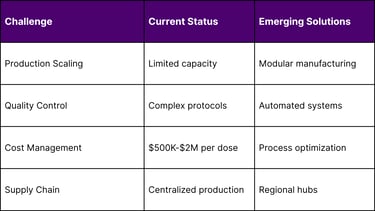

Manufacturing and Commercialization Dynamics

Manufacturing Challenges and Solutions

Cost-Effectiveness Models

Health Economic Considerations:

Lifetime Treatment Costs: $3-8 million for chronic care

Gene Therapy Cost: $1-3 million one-time treatment

QALY Analysis: 15-25 quality-adjusted life years gained

Payer Acceptance: Outcome-based payment models emerging

Regional Market Analysis

North America: Innovation Leader

Market Characteristics:

Market Share: 45% ($168.5 billion by 2030)

Regulatory Advantage: FDA fast-track programs

Investment Hub: 60% of global VC funding

Clinical Infrastructure: Leading trial capabilities

Key Growth Drivers:

Advanced healthcare infrastructure

Strong intellectual property protection

High healthcare spending per capita

Government research funding (NIH)

Europe: Regulatory Harmonization

Market Characteristics:

Market Share: 32% ($119.8 billion by 2030)

Regulatory Framework: EMA centralized procedures

Healthcare Integration: Cross-border collaboration

Research Excellence: Academic-industry partnerships

Asia-Pacific: Emerging Powerhouse

Market Characteristics:

Market Share: 18% ($67.4 billion by 2030)

Growth Rate: Fastest at 14.2% CAGR

Manufacturing Hub: Cost-effective production

Population Genetics: Unique disease prevalence patterns

Investment and Partnership Landscape

Venture Capital Trends

2024 Investment Highlights:

Total Gene Therapy Investment: $8.4 billion

Average Series A: $35 million

Late-Stage Funding: $120 million average

IPO Activity: 15 gene therapy companies public

Strategic Partnerships

Big Pharma Acquisitions (2023-2025):

Roche-Spark Therapeutics: $4.8 billion (2019, impact continuing)

Novartis-AveXis: $8.7 billion (2018, market expansion)

Biogen Partnerships: Multiple $1B+ collaborations

Gilead-Kite Integration: CAR-T and gene therapy synergies

Government Funding Initiatives

National Institutes of Health (NIH):

SOMATIC Program: $190 million for gene editing

COMMON Fund: $100 million for rare disease research

NCATS TRND: Therapeutic development support

FDA Critical Path: Regulatory guidance development

Competitive Landscape Analysis

Market Leaders

Novartis: Comprehensive gene therapy portfolio

Zolgensma success driving growth

Manufacturing capacity expansion

Global market penetration strategy

Pipeline diversification across disease areas

Sarepta Therapeutics: DMD focus

Multiple gene therapy approaches

Regulatory expertise in accelerated approvals

Patient advocacy partnerships

International expansion initiatives

Biogen: Neurological disorder specialization

Spinraza market leadership

Gene therapy pipeline development

Manufacturing partnerships

Digital health integration

Emerging Companies

Platform Technology Leaders:

Editas Medicine: CRISPR applications

Intellia Therapeutics: In vivo gene editing

Alnylam Pharmaceuticals: RNAi therapeutics

Solid Biosciences: Duchenne muscular dystrophy

Regulatory Pathway Evolution

FDA Guidance Development

Recent Guidance Documents (2024-2025):

Gene therapy manufacturing quality standards

Clinical trial design for rare disease applications

Long-term follow-up requirements

Combination product regulations

International Harmonization

ICH Guidelines Progress:

Quality considerations for gene therapies

Clinical development strategies

Pharmacovigilance requirements

Regulatory convergence initiatives

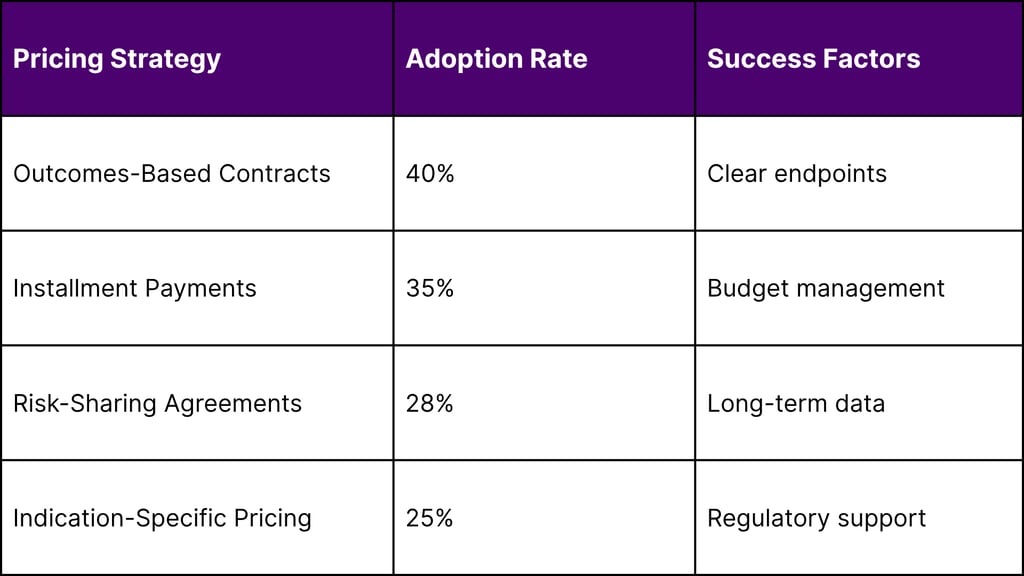

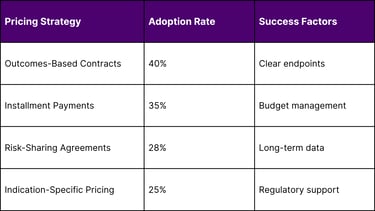

Market Access and Pricing Strategies

Value-Based Pricing Models

Payer Engagement Strategies

Health Technology Assessment (HTA) Considerations:

Early engagement with payer organizations

Real-world evidence generation plans

Budget impact modeling

Patient-reported outcome measures

Technology Integration and Innovation

CRISPR and Gene Editing Advances

Technical Breakthroughs:

Base Editing: Precision without double-strand breaks

Prime Editing: Targeted insertions and corrections

Epigenome Editing: Regulatory element modifications

Delivery Systems: Lipid nanoparticles and AAV vectors

Manufacturing Innovation

Process Improvements:

Continuous Manufacturing: Reduced production times

Quality by Design: Built-in quality systems

Automation: Reduced human error and costs

Analytical Methods: Real-time release testing

Challenges and Risk Mitigation

Technical Challenges

Delivery Systems:

Vector immunogenicity concerns

Tissue-specific targeting requirements

Dosing optimization needs

Long-term safety monitoring

Manufacturing Complexity:

Scale-up difficulties

Quality control requirements

Supply chain management

Regulatory compliance costs

Market Access Barriers

Pricing Pressure:

Payer budget constraints

Health technology assessment requirements

International reference pricing

Biosimilar competition emergence

Future Market Projections

Short-Term Outlook (2025-2027)

Market Drivers:

25+ gene therapy approvals expected

Manufacturing capacity doubling

Cost reduction initiatives

Payer acceptance increasing

Growth Catalysts:

Platform technology maturation

Combination therapy approaches

Digital health integration

Global market expansion

Medium-Term Projections (2027-2030)

Market Evolution:

Outpatient treatment models

Biosimilar competition beginning

Outcome-based pricing standard

Preventive applications emerging

Technology Convergence:

AI-driven drug discovery acceleration

Personalized gene therapy approaches

Multi-modal treatment strategies

Digital biomarker integration

Long-Term Vision (2030+)

Market Transformation:

Gene therapy as standard of care

Preventive genetic interventions

Global access programs established

Curative treatments for most rare diseases

Innovation Frontiers:

In vivo gene editing therapeutics

Synthetic biology applications

Tissue engineering integration

Regenerative medicine convergence

Strategic Recommendations

For Pharmaceutical Companies

Investment Priorities:

Manufacturing Capabilities: Build or acquire gene therapy production facilities

Platform Technologies: Invest in versatile delivery systems and manufacturing platforms

Regulatory Expertise: Develop specialized rare disease regulatory capabilities

Patient Access Programs: Create innovative financing and access solutions

Partnership Strategies:

Academic medical center collaborations for clinical development

Patient advocacy partnerships for disease education

Technology platform licensing agreements

International distribution partnerships

For Biotech Companies

Development Focus:

Differentiated Mechanisms: Target underserved rare disease populations

Platform Approaches: Develop technologies applicable across multiple diseases

Manufacturing Partnerships: Secure production capacity early

Regulatory Strategy: Engage agencies early for guidance

Commercialization Planning:

Specialty pharma partnerships for global reach

Direct patient support programs

Value-based contracting capabilities

International expansion strategies

For Investors

Investment Considerations:

Portfolio Diversification: Balance across disease areas and development stages

Platform vs. Single Asset: Evaluate scalability and applicability

Manufacturing Readiness: Assess production capabilities and partnerships

Regulatory Pathway: Consider approval timelines and requirements

Risk Assessment Factors:

Clinical development risks and mitigation strategies

Manufacturing complexity and scalability

Market access and reimbursement potential

Competitive landscape dynamics

Market Success Factors

Clinical Development Excellence

Critical Success Elements:

Natural History Studies: Understanding disease progression

Biomarker Development: Measuring treatment effects

Patient Stratification: Identifying optimal candidates

Long-term Follow-up: Demonstrating durability

Regulatory Strategy Optimization

Best Practices:

Early engagement with regulatory agencies

Adaptive trial design implementation

Real-world evidence generation

Global regulatory harmonization

Commercial Execution

Market Access Strategies:

Health economics and outcomes research

Payer engagement and education

Patient support programs

Healthcare provider training

Emerging Opportunities

Combination Therapies

Synergistic Approaches:

Gene therapy + small molecules

Gene editing + cell therapy

Multi-target gene therapy

Precision medicine combinations

Digital Health Integration

Technology Applications:

Remote patient monitoring

Digital biomarkers

Artificial intelligence diagnostics

Telemedicine delivery

Global Market Expansion

Emerging Markets:

Asia-Pacific regulatory development

Latin America access programs

Middle East partnership opportunities

Africa humanitarian initiatives

Risk Factors and Mitigation Strategies

Technical Risks

Manufacturing Challenges:

Risk: Production scaling difficulties

Mitigation: Modular manufacturing approaches and strategic partnerships

Safety Concerns:

Risk: Long-term adverse effects

Mitigation: Comprehensive safety monitoring and risk management plans

Commercial Risks

Market Access Barriers:

Risk: Payer resistance to high prices

Mitigation: Value-based pricing and outcome guarantees

Competitive Threats:

Risk: Multiple therapies for same indication

Mitigation: Differentiation through efficacy, safety, or convenience

Conclusion

The rare diseases treatment market stands at an unprecedented inflection point, with gene therapy driving a transformation that will reshape the pharmaceutical industry over the next decade. The convergence of scientific breakthroughs, regulatory support, and commercial opportunity creates a $374.4 billion market opportunity by 2030.

The success stories emerging from spinal muscular atrophy, Duchenne muscular dystrophy, and inherited retinal dystrophies demonstrate that gene therapy can deliver not just clinical benefits, but also substantial commercial returns. As manufacturing scales, costs decrease, and access expands, gene therapy will transition from experimental treatment to standard of care across hundreds of rare diseases.

For stakeholders across the ecosystem, the message is clear: the gene therapy gold rush is not a future opportunity—it is happening now. Organizations that can navigate the complex development landscape, build scalable manufacturing capabilities, and create innovative market access solutions will capture the most significant value in this transformative market.

The rare disease community has waited decades for effective treatments. Gene therapy is delivering on that promise while creating one of the most lucrative pharmaceutical market opportunities of our time. The question for industry participants is not whether to engage, but how quickly and effectively they can scale their participation in this revolutionary market transformation.

The convergence of unmet medical need, scientific capability, and commercial opportunity has created a perfect storm for gene therapy success in rare diseases. The gold rush is underway, and the prospectors who stake their claims today will reap the rewards for decades to come.

FAQs

1. What is driving the explosive growth of the rare disease market?

The market is projected to grow from $195.2B (2024) to $374.4B by 2030 (11.6% CAGR), driven by gene therapy breakthroughs, favorable regulatory incentives (like FDA’s Orphan Drug Act), and massive venture capital investments.

2. How is gene therapy changing the treatment landscape for rare diseases?

Gene therapy offers the potential for one-time, curative treatments targeting the genetic root cause of diseases, replacing the traditional model of lifelong symptom management.

3. Which rare diseases are seeing the biggest impact from gene therapy?

Top areas include:

Spinal Muscular Atrophy (SMA)

Duchenne Muscular Dystrophy (DMD)

Inherited retinal diseases

Beta-thalassemia and Sickle Cell Disease

These indications lead in both FDA approvals and clinical trial momentum.

4. What are the biggest regulatory advantages for orphan drugs and gene therapies?

Key benefits include:

7–10 years market exclusivity

Fast-track designations

Tax credits and waived fees

EMA centralized procedures in Europe

These reduce time-to-market and improve commercial feasibility.

5. How many gene therapies are currently approved?

As of 2025, FDA has approved several gene therapies including:

Zolgensma (SMA)

Luxturna (retinal dystrophy)

Spinraza and Elevidys (neurological disorders)

45+ new FDA submissions are expected by 2026.

6. What are the primary challenges in gene therapy commercialization?

Major hurdles include:

High manufacturing costs ($500K–$2M per dose)

Scalability of vector production

Complex regulatory compliance

Access and pricing models for one-time therapies

7. How are payers responding to the high cost of gene therapies?

Payers are adopting value-based pricing models, including:

Installment payment plans

Outcome-based contracts

Risk-sharing agreements

These align cost with clinical benefit over time.

8. Which regions are leading this market?

North America leads with 45% share due to FDA pathways and investment.

Europe follows with regulatory harmonization and public reimbursement.

Asia-Pacific is the fastest-growing region with 14.2% CAGR due to local manufacturing hubs and population-specific disease prevalence.

9. What is the investor sentiment around gene therapy?

Very bullish. In 2024 alone:

$8.4B was invested globally

Late-stage Series B/C rounds averaged $120M

IPOs surged with 15 gene therapy companies going public

10. What’s the long-term outlook for gene therapy in rare diseases?

By 2030+, gene therapy is expected to become:

The standard of care for many monogenic diseases

A curative solution replacing chronic therapies

A cornerstone of personalized, precision medicine

References

U.S. Food and Drug Administration (FDA) – Drug Approvals and Databases

European Medicines Agency (EMA) – Regulatory Guidelines and Approvals

National Institutes of Health (NIH) – Research Portfolio Online Reporting Tools (RePORT)

World Health Organization (WHO) – Rare Disease Statistics and Global Health Estimates

Peer-Reviewed Clinical Research Publications

Navigation

© 2026 FyreIgnis Market Research. All rights reserved.

Legal

info@fyreignismarketresearch.com

India