Gene Therapy’s Pricing Paradox

The global healthcare ecosystem in March 2026 stands at a historic crossroads, defined by the maturation of regenerative medicine and the subsequent collapse of traditional pharmaceutical reimbursement frameworks. The advent of cell and gene therapies (CGTs) has introduced a profound pricing paradox: while these interventions offer the unprecedented potential for one-time, life-altering cures, their multimillion-dollar upfront costs challenge the liquidity and long-term solvency of even the most robust healthcare systems. As of mid-March 2026, the industry is witnessing a shift away from simple discount-based pricing toward a sophisticated infrastructure of outcomes-based agreements (OBAs) and annuity-style installments. This evolution is driven by the necessity of market access for nearly 20 therapies now commercially available in the United States and a pipeline that expects 20 to 30 new regulatory filings annually in Europe alone.

The current landscape is punctuated by the full-scale implementation of the Centers for Medicare & Medicaid Services (CMS) Cell and Gene Therapy Access Model, which, as of March 2026, has expanded to include 34 state participants representing approximately 84% of the Medicaid beneficiaries living with sickle cell disease (SCD). Simultaneously, the European Union is navigating the early implementation phases of the 2025 Biotech Act, a legislative effort designed to harmonize regulatory pathways and bridge the late-stage capital gap that has historically forced European innovators to seek American or Asian capital markets. This report provides an exhaustive analysis of the financing mechanisms, regulatory shifts, and economic implications of the gene therapy market as it exists in the first quarter of 2026.

The Valuation Conflict: Cost-Effectiveness vs. Commercial Viability

The pricing paradox is fundamentally rooted in the structural gap between value-based prices determined by clinical benefit and cost-offsets and the prices required to sustain the commercial development of complex biological products. In traditional chronic care, a patient represents a recurring revenue stream for manufacturers and a predictable, amortized expense for payers. Gene therapies disrupt this by condensing decades of therapeutic value into a single administration.

Economic modeling in early 2026 utilizing risk-adjusted net present value (rNPV) highlights this discrepancy. To attract private investment, therapies often require a price point exceeding $1 million, especially when manufacturing costs are estimated near $200,000 per dose. However, many national health systems, particularly in the European Union, operate under willingness-to-pay thresholds that would ideally price these same therapies below $500,000. This "feasibility gap" has necessitated the development of innovative financing models that can bridge the divide between what a system can afford upfront and the total clinical value provided over a patient's lifetime.

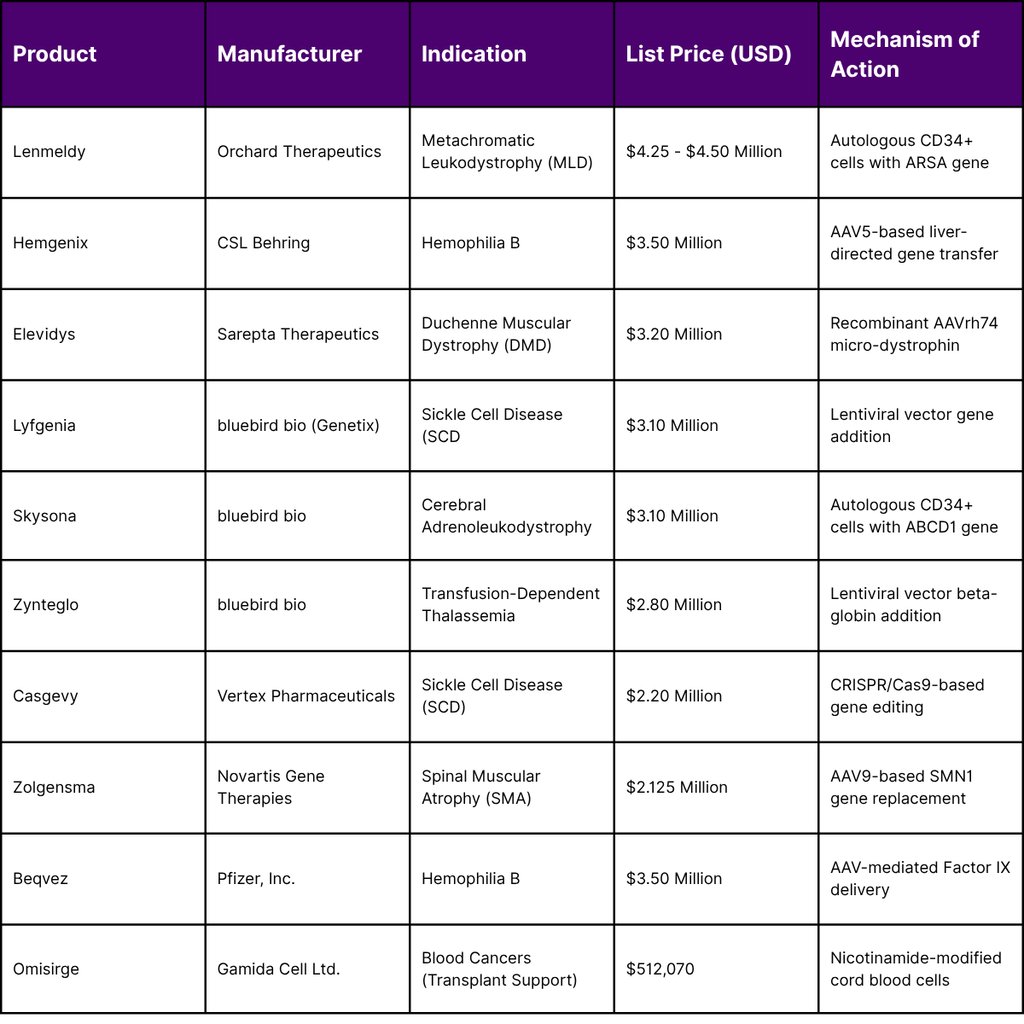

Table 1: Comparative Pricing and Indications for Leading Gene Therapies (March 2026)

The data suggests that the "standard" price for a transformative gene therapy has stabilized between $2 million and $3.5 million, with outliers like Lenmeldy pushing the boundary toward $4.5 million. Payers justify these expenditures by comparing them to the cumulative cost of conventional treatment. For example, prophylactic treatment for Hemophilia B costs approximately $788,491 per year. Over five years, the total cost of conventional care reaches $3.9 million, making a one-time payment of $3.5 million for Hemgenix economically superior.

The CMS Cell and Gene Therapy (CGT) Access Model: A New Federal Standard

A defining development of early 2026 is the operational maturity of the CMS Cell and Gene Therapy (CGT) Access Model. This multi-year, voluntary program marks the first instance of the U.S. federal government negotiating outcomes-based agreements (OBAs) on behalf of state Medicaid agencies. The model initially targets sickle cell disease, a condition affecting 100,000 Americans, of whom 50% to 60% are enrolled in Medicaid.

Operational Mechanics and State Participation

Under the CGT Access Model, CMS negotiates key terms with manufacturers specifically Genetix Biotherapeutics (formerly bluebird bio) for Lyfgenia and Vertex Pharmaceuticals for Casgevy. These terms include standardized access policies, pricing discounts, and outcomes-based rebates. Participating states, which now include Maryland, Mississippi, Massachusetts, and 31 others, implement these agreements as supplemental rebate agreements (SRAs).

The model’s performance period follows a "rolling start" that began in January 2025 and reached its final state-onboarding milestone in January 2026. States like Mississippi and Maryland, which joined officially on January 1, 2026, are now actively utilizing federal funding to support the high-complexity patient journey required for gene therapy.

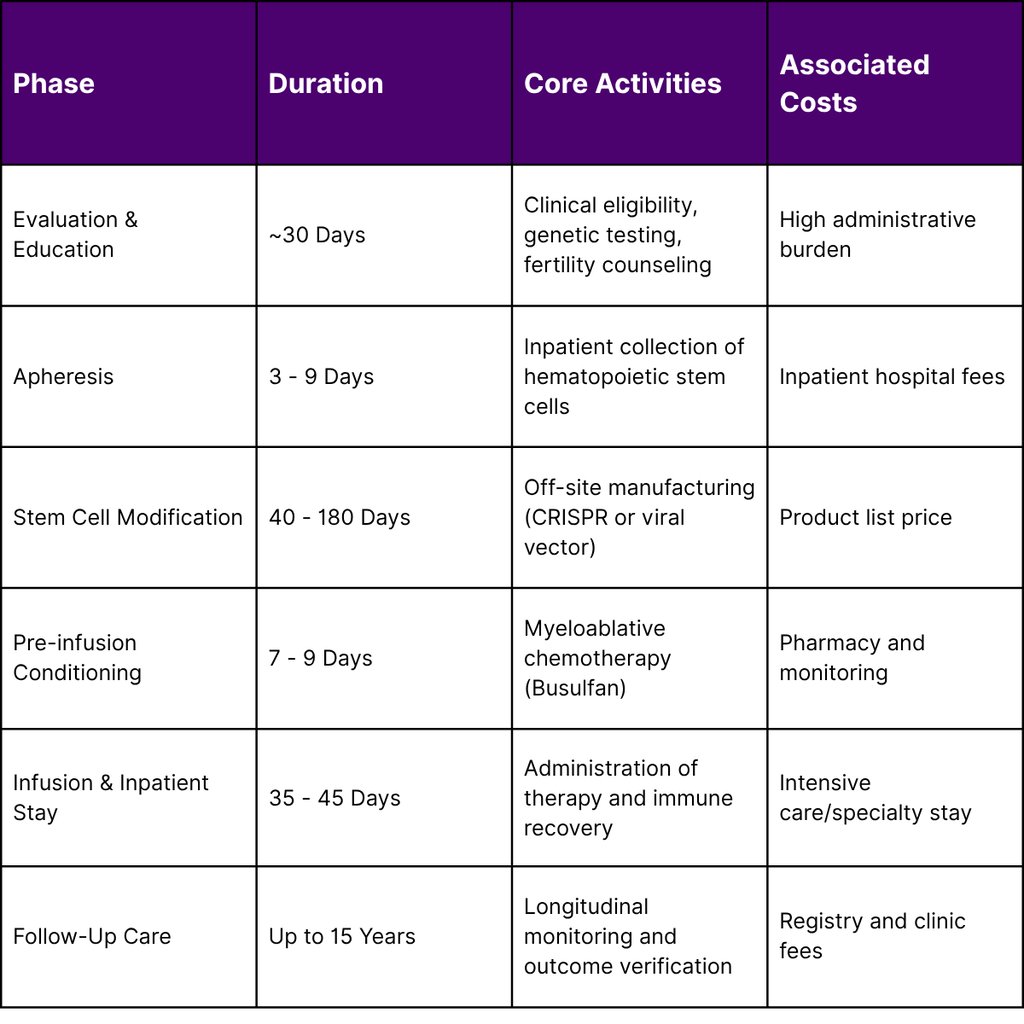

Table 2: The Gene Therapy Patient Journey and Care Coordination (SCD Focus)

This journey is not merely a clinical process but an economic one. CMS requires participating manufacturers to cover specific ancillary costs, such as fertility preservation, travel, and lodging, to ensure equitable access for Medicaid beneficiaries who might otherwise be unable to afford the indirect costs of treatment.

Outcomes-Based Rebates and Data Requirements

The financial integrity of the CGT Access Model relies on the verification of clinical outcomes. If a therapy fails to deliver the promised therapeutic benefits such as a reduction in vaso-occlusive crises (VOCs) the manufacturer is contractually obligated to reimburse the state Medicaid program.

To facilitate this, CMS utilizes the Transformed Medicaid Statistical Information System (T-MSIS) and partnerships with the Center for International Blood and Marrow Transplant Research (CIBMTR). Providers must submit extensive data to the CIBMTR registry, including:

Clinical Indicators: Percentages of fetal hemoglobin (HbF) and laboratory values demonstrating genetic correction.

Patient-Reported Outcomes (PROs): Standardized surveys assessing anxiety, depression, pain, fatigue, and sleep disturbance.

Verification Timeline: PRO surveys are administered at 30, 100, and 180 days post-infusion, with annual follow-ups for up to five years.

The European Context: The 2025 Biotech Act and Innovation Strategy

While the United States focuses on Medicaid-led negotiation, the European Union is implementing the Biotech Act, proposed in late 2025 and entering a critical transition phase in March 2026. The EU faces a distinct crisis: between 2019 and 2025, 66 out of 67 European biotech firms chose to list on non-EU stock exchanges due to a lack of late-stage capital. The Biotech Act seeks to rectify this by repositioning the EU as a global hub for Advanced Therapy Medicinal Products (ATMPs).

Key Pillars of the EU Biotech Act

The Act introduces seven pillars of reform, with several directly impacting gene therapy financing and market access:

Health Biotechnology Investment Pilot: Developed with the European Investment Bank (EIB) Group, this facility offers equity and venture debt to bridge the funding gap for Phase III trials and manufacturing scale-up.

Strategic Project Designation: High-impact projects can receive "Strategic Project" status, unlocking fast-tracked permits (max 8-10 months) and priority access to EU funding.

Intellectual Property Incentives: The Act proposes a 12-month extension to Supplementary Protection Certificates (SPCs) for innovative biotech products, provided a significant manufacturing step occurs within the Union.

Regulatory Sandboxes: For novel products that fall between existing categories (e.g., combined device-biotech therapies), sandboxes allow for controlled testing and evidence generation outside traditional pathways.

These measures are designed to address the "innovation gap" where the EU currently holds only a 7% share of global venture capital in health biotech, compared to 63% in the U.S..

The UK's Managed Access and the Innovative Medicines Fund (IMF)

In the United Kingdom, the Innovative Medicines Fund (IMF), established in June 2022, has become the primary vehicle for early access to gene therapies. As of March 2026, the IMF has significantly ramped up its expenditure, spending £18 million in the current financial year to date a sharp increase from the £2 million spent in previous years.

The IMF operates by providing time-limited funding for medicines while further data is collected to address uncertainties identified by the National Institute for Health and Care Excellence (NICE). After a managed access period of up to five years, NICE conducts a final appraisal to determine if the therapy should move to routine commissioning. Furthermore, as of April 2026, NICE will implement a revised cost-effectiveness threshold of £25,000 to £35,000 per QALY, up from the long-standing £20,000 to £30,000 range, as part of the UK-US pharmaceuticals trade deal.

Annuity-Style Payment Models: Solving the Budget Impact Challenge

The "Pricing Paradox" is most acutely felt at the moment of treatment, where a payer must absorb the full cost of a multimillion-dollar therapy. Annuity-style payment models also known as spread payments or installments are becoming essential for market access by aligning the timing of payment with the duration of the clinical benefit.

The Mechanics of Medical Annuities

Annuity models allow payers to spread the cost of a therapy over a fixed period, typically between three and seven years. In 2026, several hybrid models have emerged where payments are not only spread out but are also contingent on the patient remaining in a specific health state (e.g., transfusion-free or crisis-free).

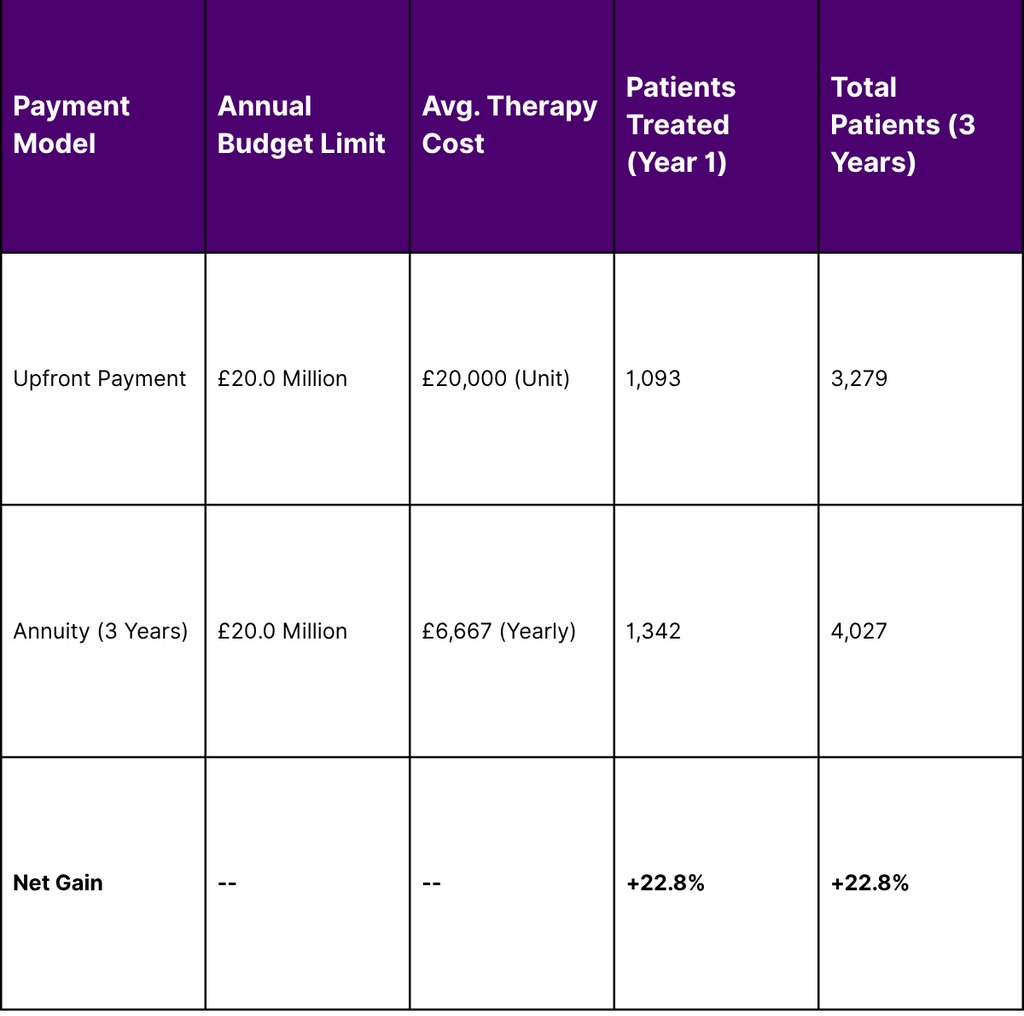

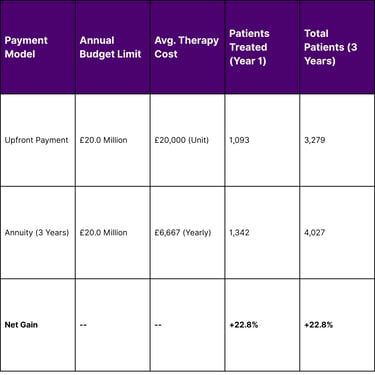

Table 3: Economic Impact of Annuity Payments on Patient Access (Simulation)

The simulation data demonstrates that by utilizing annuity-based payments, health systems can increase patient access by nearly 23% without exceeding annual net budget impact thresholds. This is particularly critical for conditions with large prevalent populations, where a sudden influx of eligible patients could otherwise trigger budget caps and restrict access.

Legislative and Policy Disruptions: The OBBBA Impact

The financing of gene therapies in the United States is further complicated by the "One Big Beautiful Bill Act" (OBBBA), or Public Law 119-21, signed in July 2025.34 This massive budget reconciliation package contains provisions that simultaneously provide new infrastructure funding while imposing significant fiscal constraints on Medicaid.

Medicaid Financing and Provider Taxes

The OBBBA introduces strict new limits on state-directed payments (SDPs) and the use of provider taxes to fund the state share of Medicaid.34 Beginning October 1, 2026, states are effectively prohibited from increasing revenue through health care-related taxes in almost all instances. This is a major concern for the gene therapy market, as many states have historically relied on these taxes to generate the funds necessary to pay for high-cost specialty drugs.

Eligibility and Redeterminations

The law also imposes new administrative hurdles for Medicaid expansion enrollees a group that includes many adult patients with sickle cell disease:

Work Requirements: Effective January 1, 2027, non-disabled adults must work or engage in qualifying community activities for 80 hours per month.

Six-Month Redeterminations: States must now redetermine eligibility for expansion enrollees every six months, doubling the frequency of the process and increasing the risk of coverage lapses.

Asset and Data Matching: States are required to conduct quarterly checks of the Social Security Death Master File (DMF) and use the PARIS system to identify multi-state enrollment.

These changes are estimated to reduce state Medicaid budgets by $665 billion over the next decade. For the gene therapy sector, this translates to a more precarious funding environment where administrative churn could interrupt the long-term monitoring required for outcomes-based payments.

State-Level Case Studies: Implementation in 2026

As of March 2026, states are navigating the intersection of federal models and state-specific legislative mandates. The diversity of approaches provides a blueprint for how different regions are managing the Pricing Paradox.

Maryland: The Expansion of Local Access

Maryland Medicaid officially joined the federal CGT Access Model in late 2025, with enhanced rebates and financial protections taking effect on January 1, 2026. The state currently identifies 3,000 Medicaid participants with SCD, although not all meet the clinical criteria for gene therapy. Maryland has focused on a "hub-and-spoke" model, authorizing two primary centers the University of Maryland Medical Center and Children's National Hospital to administer the therapies while using federal funding to support patient travel and housing.

Mississippi: Focus on Workforce and Navigation

Mississippi, another participant in the CMS model, has utilized its Cooperative Agreement funding to create dedicated patient support roles. By March 13, 2026, the Mississippi Division of Medicaid is closing applications for Program Coordinators tasked specifically with guiding members through the complex 15-year post-infusion journey. This emphasizes the transition of Medicaid agencies from simple insurance payers to active care managers.

Massachusetts: Primary Care and Sub-Capitation

In Massachusetts, the 2026 landscape is defined by the "Senior Care Options" (SCO) eligibility changes and a focus on value-based primary care. While participating in the federal gene therapy model, Massachusetts is also proposing advanced primary care payment models that utilize prospective, capitated payments. This shift toward capitation at the primary care level is designed to create a more stable foundation for managing the chronic complications of SCD before and after curative gene therapy.

Future Outlook: Expansion Beyond Sickle Cell Disease

The success of the SCD gene therapy model in 2026 is viewed as a pilot for broader applications. CMS has already indicated that it may modify the model in the future to cover other high-cost, high-impact therapies for conditions like Hemophilia, Duchenne Muscular Dystrophy, and potentially certain CAR-T oncology treatments.

Emerging Technologies and Cost Pressures

The clinical pipeline remains robust. Looking into late 2026 and 2027, the FDA and EMA are preparing for several major milestones:

Fabry's Disease: Prospective gene therapies are on the near horizon for 2026.

Genome Editing: New draft guidance from the FDA, released in February 2026, aims to remove regulatory barriers for genome editing products targeting different mutations within a single gene, potentially allowing them to be evaluated under a master protocol.

Bioprinting and RNA Therapies: The European Commission is prioritizing regulatory science for patient-centered health technologies, including RNA-based therapies and regenerative medicine.

By 2030, one study estimates that between 54 and 74 cell and gene therapies will be approved, with over 340,000 patients treated annually. Total annual spending on these therapies is projected to reach $25.3 billion by the end of 2026 alone.

Conclusion: The New Economic Social Contract

The Pricing Paradox of gene therapy is not merely a financial problem but a challenge to the existing social contract of healthcare. In 2026, the resolution of this paradox lies in the shift from transactional to longitudinal relationships. Payers are no longer just buyers of drugs; they are investors in health outcomes. Manufacturers are no longer just sellers of products; they are long-term partners in patient wellness.

Innovative financing models OBAs, annuities, and federalized negotiation have provided the tools necessary to make cures accessible today while safeguarding the fiscal sustainability of the future. However, as legislative reforms like the OBBBA continue to reshape the Medicaid landscape, the industry must remain vigilant in ensuring that administrative complexity does not become a new barrier to the very cures that science has finally made possible.

Frequently Asked Questions (FAQ)

Q1: How does the CMS CGT Access Model differ from standard Medicaid drug purchasing?

In standard purchasing, states pay for a drug regardless of the outcome, often receiving a fixed discount. In the CGT Access Model, CMS negotiates on behalf of all participating states to tie the final price to specific clinical outcomes. If the therapy fails (e.g., if an SCD patient has a vaso-occlusive crisis after treatment), the manufacturer must provide an additional rebate to the state.

Q2: What is an "annuity-style" payment in the context of gene therapy?

This model allows the high cost of a gene therapy (e.g., $3 million) to be paid in smaller, annual installments over several years (often 5 to 7 years). These payments can be "performance-linked," meaning the payer only continues the installments if the therapy remains effective.

Q3: Are manufacturers required to cover patient travel and lodging?

Under the CMS CGT Access Model for sickle cell disease, participating manufacturers are required to pay for a defined scope of fertility preservation services and support for ancillary services, including travel and lodging, to address access barriers for Medicaid beneficiaries.

Q4: How does the "One Big Beautiful Bill Act" (OBBBA) affect gene therapy?

The OBBBA (Public Law 119-21) limits the ability of states to use provider taxes to fund Medicaid and increases the frequency of eligibility redeterminations. These measures could reduce the funds available to states to pay for gene therapies and potentially cause patients to lose coverage during the 15-year follow-up period.

Q5: What data is collected to verify that a gene therapy has worked?

CMS and registries like the CIBMTR collect laboratory values (such as HbF levels) and patient-reported outcomes (surveys on pain, anxiety, and function). These are collected at 30, 100, and 180 days, and then annually to ensure the "cure" is durable.

References

American Society of Hematology. (2026). Comments to CMS on Patient Protection and Affordable Care Act benefit and payment updates.

Association of American Medical Colleges. (2026). The return on investment of NIH research funding: 2026 annual report. United for Medical Research.

Centers for Medicare & Medicaid Services. (2025). Announcement of calendar year 2026 Medicare Advantage capitation rates and Part C and Part D payment policies.

Centers for Medicare & Medicaid Services. (2025). Cell and Gene Therapy (CGT) Access Model: State request for applications (RFA).

Centers for Medicare & Medicaid Services. (2026). Frequently asked questions: Cell and Gene Therapy (CGT) Access Model.

European Commission. (2025). Proposal for a Biotech Act: Building a world-leading health biotech industry.

Government Accountability Office. (2025). GAO’s FY 2025 report card: What we did to improve federal programs and save billions.

Maryland Department of Health. (2025). Maryland joins federal model to improve access and savings to lifesaving sickle cell treatments.

Mississippi Division of Medicaid. (2026). Cell and Gene Therapy (CGT) Access Model participation updates.

National Institute for Health and Care Excellence. (2025). NICE confirms changes to cost-effectiveness thresholds beginning April 2026.

U.S. Food and Drug Administration. (2026). Draft guidance: Genome editing and RNA-based therapies for rare diseases.

Vertex Pharmaceuticals. (2024). OBA negotiation and supplemental rebate framework for Casgevy.

Navigation

© 2026 FyreIgnis Market Research. All rights reserved.

Legal

info@fyreignismarketresearch.com

India