The Asia-U.S. Biotech Corridor

The $60 Billion Q1 Inflection Point: Redefining Western Oncology Pipelines

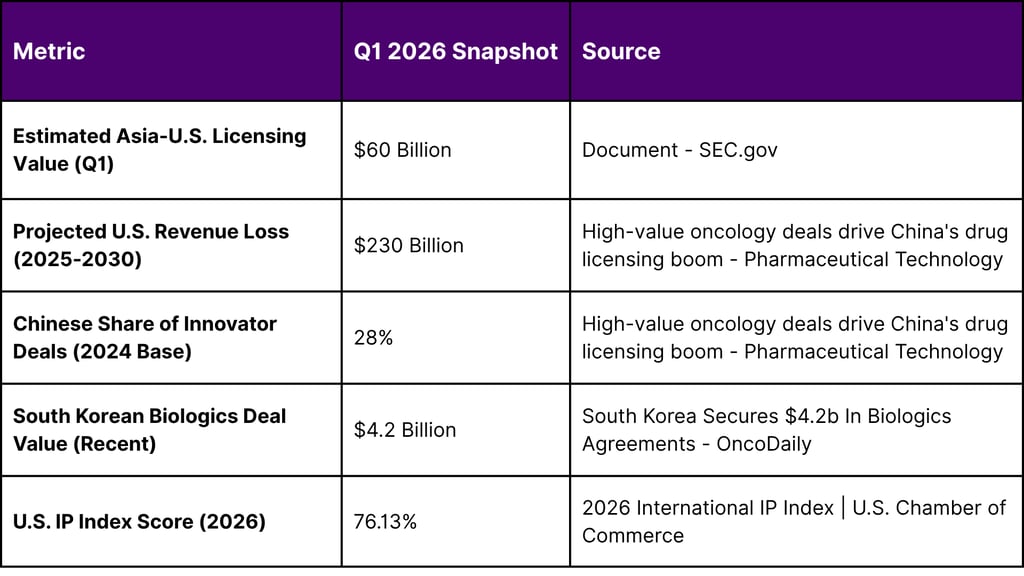

The global biopharmaceutical industry has entered a period of profound structural realignment during the first quarter of 2026. This period is characterized by an unprecedented surge in licensing activity within the Asia-U.S. biotech corridor, where the total valuation of cross-border agreements involving oncology assets from China and South Korea has reached an estimated $60 billion. This explosion in deal value is not an isolated event but rather the culmination of a decade-long maturation of Asian research and development (R&D) ecosystems, now converging with a critical "patent cliff" facing Western pharmaceutical majors.

Global pharmaceutical leaders are currently navigating a landscape where U.S. drug sales are projected to decline by approximately $230 billion between 2025 and 2030 due to the loss of exclusivity (LOE) for 190 high-earning drugs, including 69 blockbusters that generate over $1 billion annually. To mitigate these massive revenue erosions, Western firms have pivoted aggressively toward Asian innovation, specifically targeting "first-in-class" or "best-in-class" therapies in oncology, immunology, and cardiometabolic health. The first quarter of 2026 has witnessed these strategic imperatives translate into high-value transactions, with Chinese innovator deals accounting for nearly 28% of all innovator agreements signed by large pharma, representing $41.5 billion in total value in the preceding year alone.

The Convergence of Demand and Innovation

The current surge is defined by a shift from the "fast-follower" model to an era of indigenous innovation, often referred to as "Biotech 2.0". This evolution is fueled by an influx of returnee scientists to China and South Korea, bringing Western expertise to local R&D hubs to create high-quality, cost-effective therapies. Western pipelines are being revitalized by these assets, particularly in advanced therapeutic areas such as antibody-drug conjugates (ADCs), bispecific antibodies, and cell and gene therapies.

The Geopolitical and Macroeconomic Context of Early 2026

The licensing surge occurs against a backdrop of complex international trade dynamics and a volatile macroeconomic environment. According to the U.S. Bureau of Economic Analysis (BEA) and the Census Bureau, the United States saw a significant fluctuations in international trade during January 2026. The goods and services deficit increased to $61.1 billion for the three months ending in January, driven by a rise in imports while exports remained relatively stable.

Within this broader trade data, the "Charges for the use of intellectual property" (IP) metric showed a modest but consistent increase of $0.2 billion in January 2026, signaling the continued importance of cross-border licensing to the U.S. service economy. Furthermore, pharmaceutical preparations showed a decrease in both exports ($2.1 billion) and imports ($3.4 billion) in early 2026, suggesting a shift toward licensing the underlying IP rather than trading physical products a trend that directly supports the surge in licensing agreements.

Intellectual Property as a Strategic Moat

The 2026 International IP Index underscores the critical role of intellectual property frameworks in facilitating these multi-billion dollar transactions. The United States continues to lead with a score of 76.13%, while major Asian economies have demonstrated varying levels of IP policy strength. This disparity highlights why Asian biotech firms seek the protection of the U.S. legal system through licensing agreements with Western partners, ensuring that their innovations are commercialized in markets with robust enforcement mechanisms.

The Index also reveals a "troubling trend" of global stagnation in IP standards, with 27 economies registering little to no improvement in 2026. In this environment, the Asia-U.S. corridor remains a sanctuary for high-value biotech innovation, provided companies can navigate the increasing regulatory friction introduced by national security legislation.

The Chinese Innovation "2.0" Paradigm: From Replicas to Blockbusters

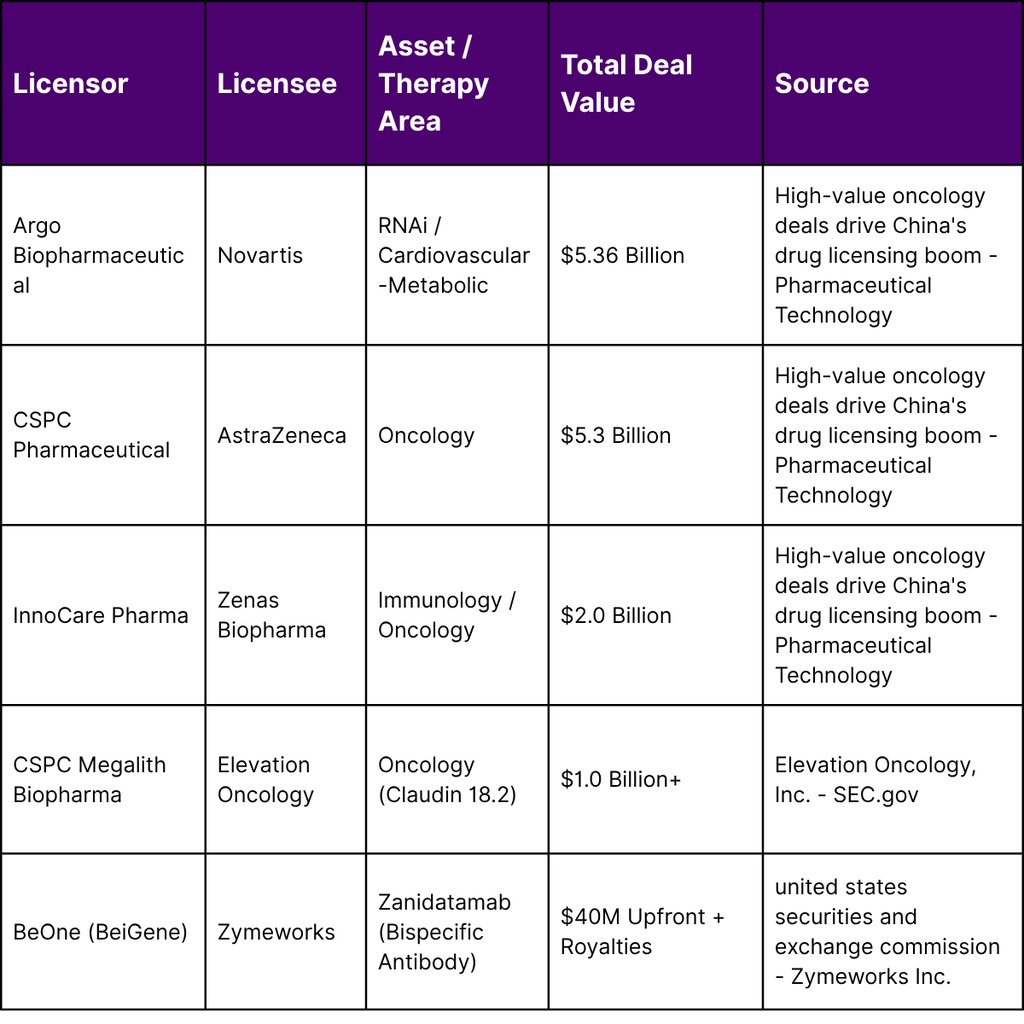

China's biopharmaceutical sector has reached a level of maturity where high-value deals worth over $500 million have transitioned from rare occurrences to industry standards.2 Between 2021 and 2024, the volume of these high-value transactions skyrocketed, with 20 such deals occurring in 2023 alone. This momentum has carried into 2026, as evidenced by major partnerships that redefine therapeutic standards.

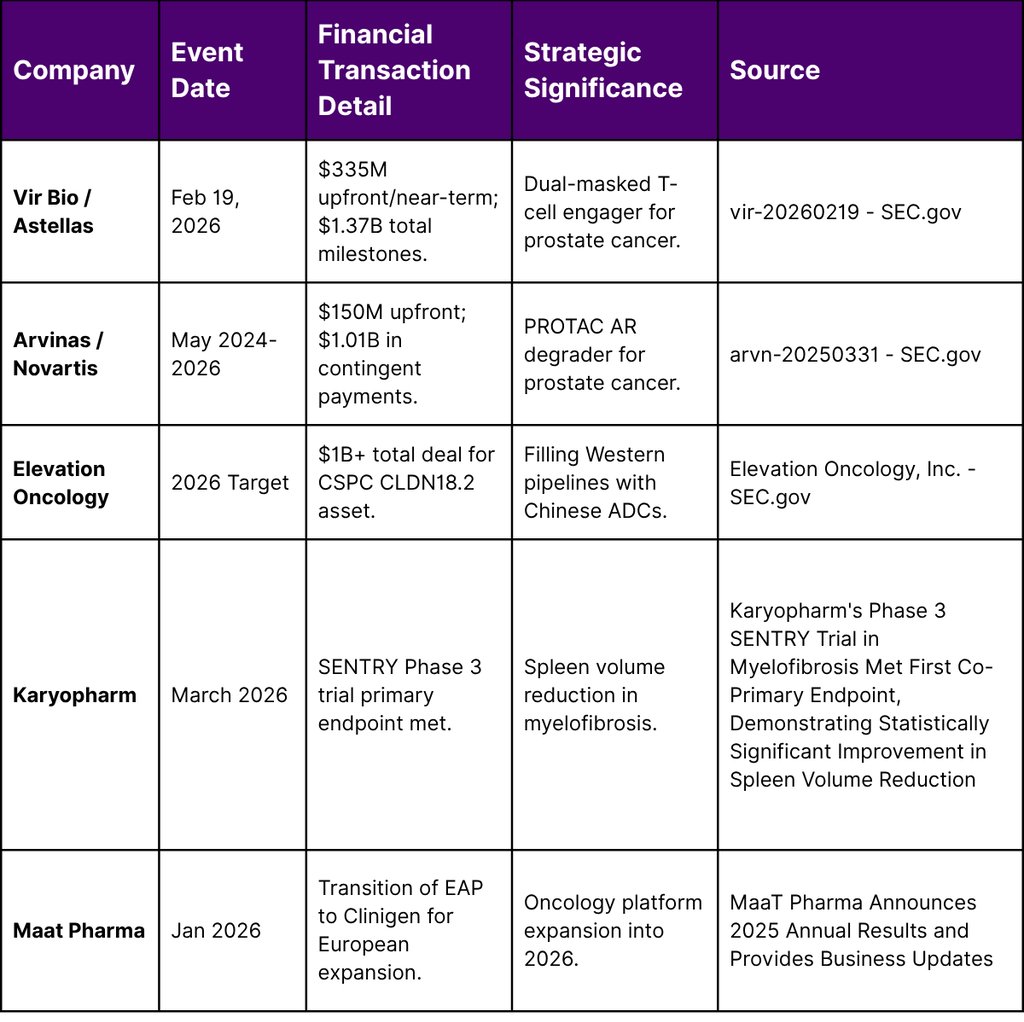

Western pharmaceutical companies are increasingly using Chinese R&D to fill gaps in their late-stage pipelines. Novartis’s $5.36 billion agreement with Argo Biopharmaceutical and AstraZeneca’s $5.3 billion partnership with CSPC Pharmaceutical represent significant bets on Chinese platform technologies. These are not mere asset purchases but long-term strategic collaborations that involve technology transfers and shared development risks.

High-Value Oncology Licensing Transactions (2024–2026)

The rise of immunotherapy and ADCs has been particularly notable. For instance, the collaboration between Zymeworks and BeOne (a subsidiary of BeiGene) for zanidatamab demonstrates how Chinese firms are now leading the clinical development and commercialization of advanced antibodies in the Asia-Pacific region, while Western partners manage the North American and European markets.

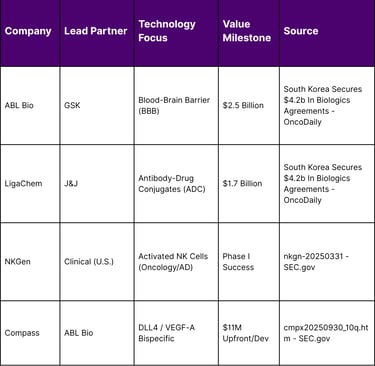

South Korea: The Advanced Biologics Powerhouse

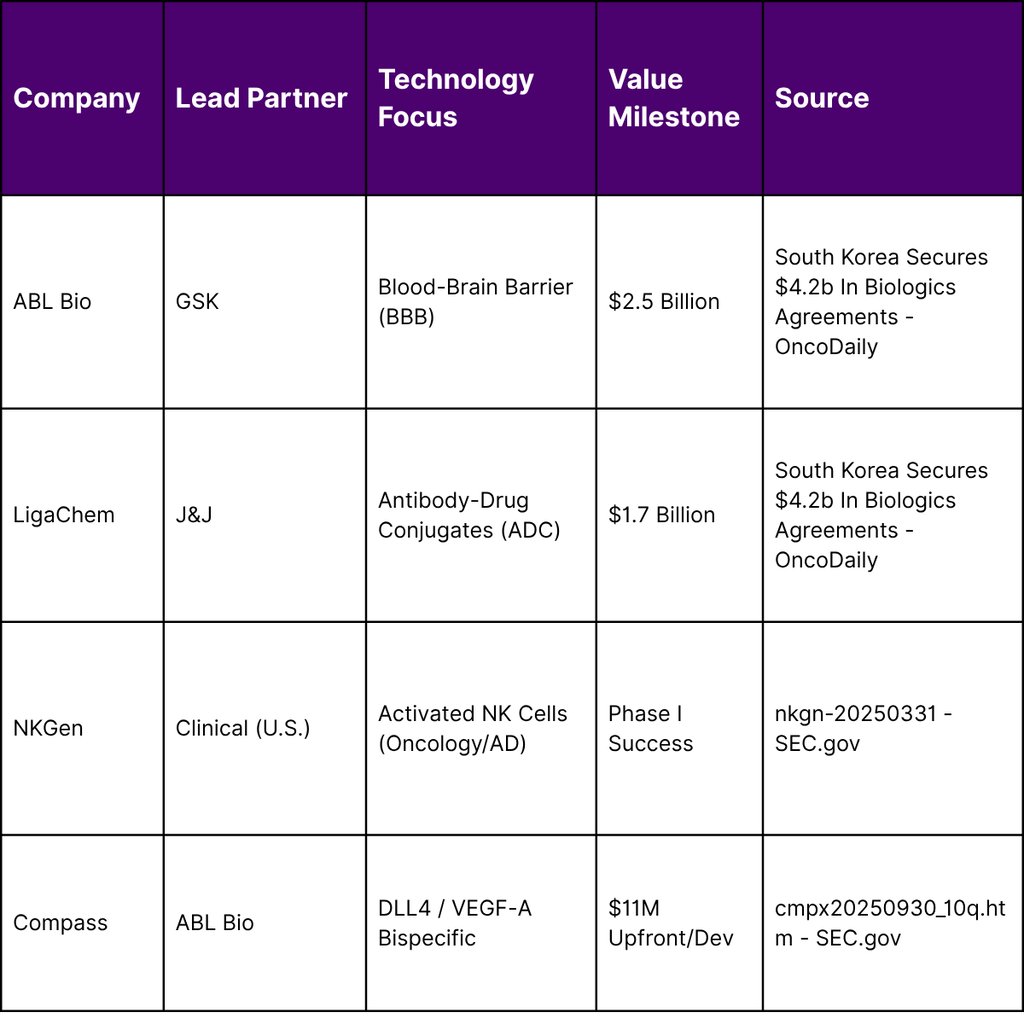

South Korea has established itself as a global leader in biologics, with its biopharma companies securing approximately $4.2 billion in agreements in the current cycle. The focus of South Korean innovation has shifted toward next-generation drug development, including treatments capable of crossing the blood–brain barrier (BBB) for neurodegenerative diseases and advanced cell and gene therapies.

Key partnerships in this sector highlight the technical depth of South Korean assets. GlaxoSmithKline’s (GSK) $2.5 billion agreement with ABL Bio is a prime example, targeting neurodegenerative diseases through a platform designed to transport therapeutic antibodies across the BBB. Similarly, LigaChem Biosciences’ $1.7 billion partnership with Johnson & Johnson (J&J) underscores the value of South Korean ADC technology in global oncology pipelines.

Clinical Momentum and South Korean Affiliates

The integration of South Korean assets is also visible in U.S. clinical trial data. NKGen, an oncology-focused firm with significant South Korean ties, presented Phase I clinical data in late 2025 showing 100% activation and expansion of natural killer (NK) cells in Alzheimer’s patients, with no treatment-related adverse events observed. This successful de-risking of assets through early-stage trials makes them highly attractive targets for the $60 billion licensing surge seen in Q1 2026.

The BIOSECURE Act of 2026: A Legal and Operational Deep Dive

While the market for Asian assets is booming, it faces a significant regulatory hurdle: the BIOSECURE Act. Signed into law on December 18, 2025, as part of the FY 2026 National Defense Authorization Act (NDAA), the Act represents a fundamental shift in U.S. policy toward the biotechnology sector. It categorizes certain biotechnology entities as "Biotechnology Companies of Concern," citing national security risks related to human multiomic and genomic data.

The Act restricts executive agencies from procuring biotechnology equipment or services from these companies and, more critically, prohibits agencies from entering into or renewing contracts with entities that use such equipment or services in the performance of federal contracts. This has created a ripple effect across the entire life sciences ecosystem, affecting everyone from prime contractors to subcontractors, research institutions, and grant recipients.

Key Adjustments in the 2026 Implementation

The final reconciled version of the BIOSECURE Act, signed in late 2025, included several industry-friendly modifications designed to soften the initial blow to global supply chains.

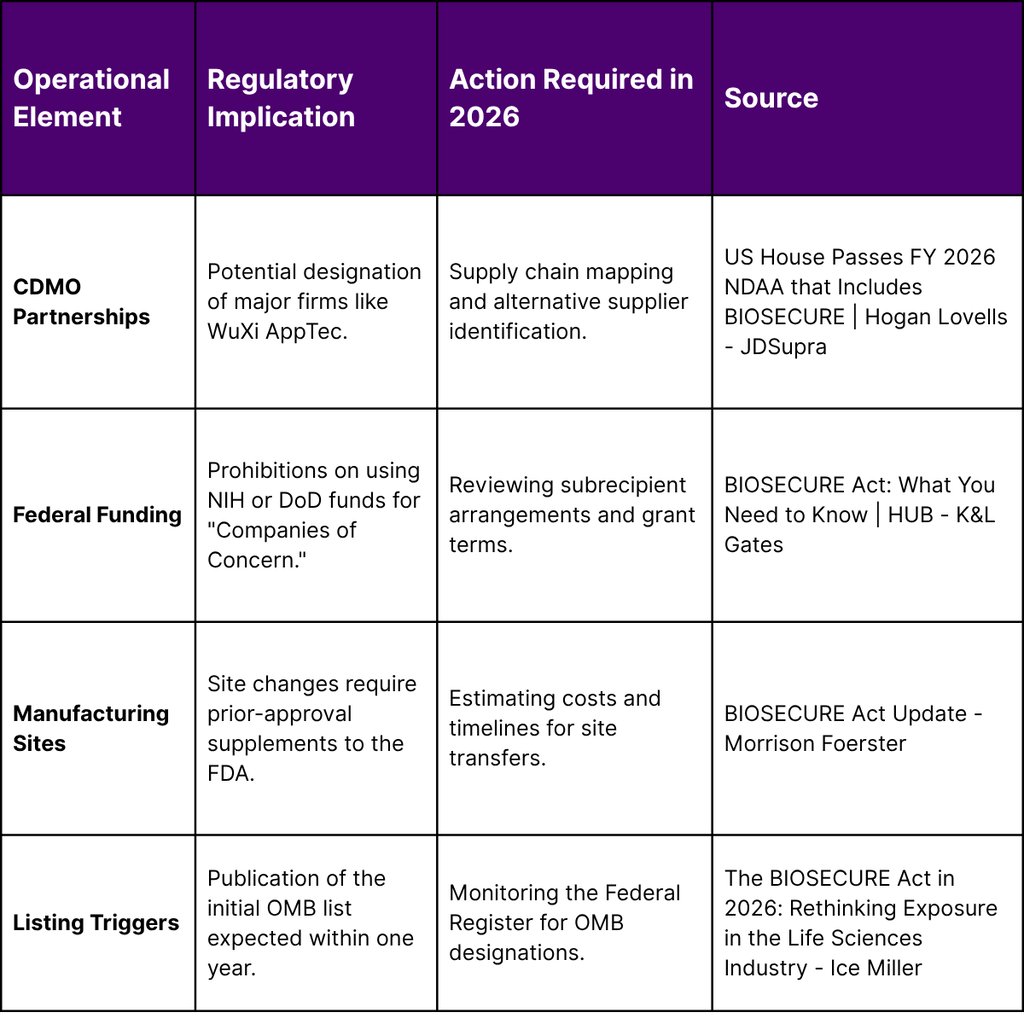

Scienter Standard: The Act now requires that a contractor "knows" (rather than just has "reason to believe") it is using prohibited biotechnology equipment or services, a change that reduces the immediate compliance burden for firms with complex, multi-layered supply chains.

Affiliate Coverage: The term "affiliate" was dropped in favor of "parents, subsidiaries, or successors," and these entities must now meet the same national security risk criteria as directly designated companies.

Transition Period: The Act provides a five-year transition period for existing contracts and grants, though this excludes companies already on the Department of Defense's 1260H list of Chinese military companies, for which restrictions take effect much sooner.

Federal Health Program Protections: The final text attempts to shield manufacturers from "collateral" impacts on Medicare Part B and Medicaid by clarifying that compliance is tied to procurement rather than reimbursement contracts.

Operational Impacts and Supply Chain Mapping

For therapeutics companies, the BIOSECURE Act necessitates a comprehensive re-evaluation of their manufacturing and research partnerships. Moving away from a designated contract development and manufacturing organization (CDMO) is not a simple task; it involves site-specific regulatory approvals, Good Manufacturing Practice (GMP) revalidation, and complex technology transfers that can take years to complete.

Larger pharmaceutical companies are generally better equipped to manage these transitions, often possessing in-house manufacturing capabilities. However, small biopharmaceutical firms are particularly vulnerable, as they often rely entirely on third-party CDMOs for their clinical trial supplies and commercial products.

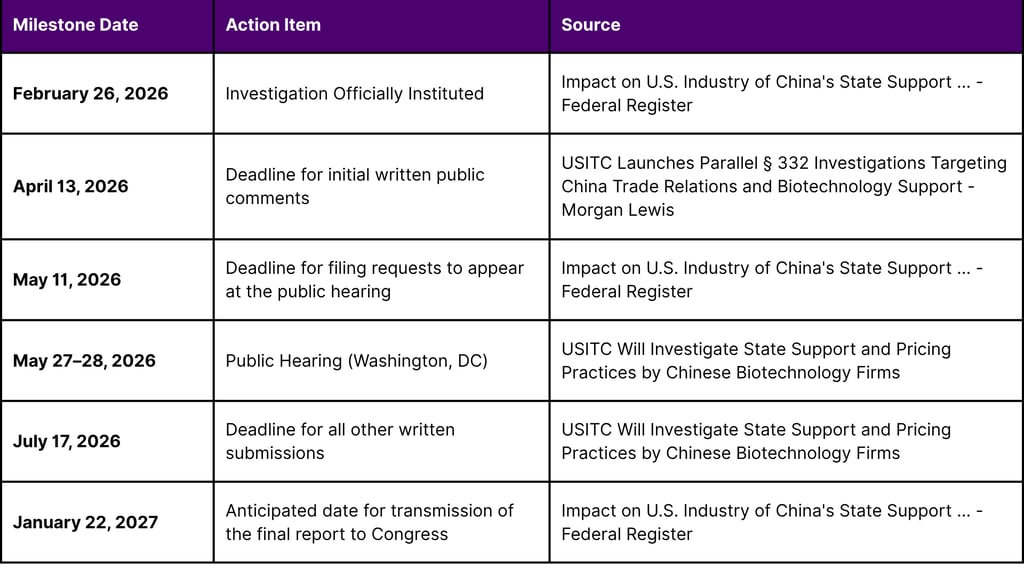

USITC Investigation No. 332-610: The Economic Security Front

Parallel to the BIOSECURE Act, the U.S. International Trade Commission (USITC) announced a fact-finding investigation in February 2026 titled "Impact on U.S. Industry of China's State Support and Pricing Practices in the Biotechnology Sector" (Inv. No. 332-610). This investigation, mandated by the Senate Appropriations Committee, aims to examine the degree of subsidization and market overcapacity by Chinese biotechnology firms and its impact on U.S. competitiveness.

The investigation covers critical areas of the biotech corridor, including genomic sequencing, synthetic biology, and active pharmaceutical ingredient (API) manufacturing. This probe is highly anticipated as its results could justify future U.S. government measures such as targeted tariffs, procurement restrictions, and outbound investment controls.

USITC Regulatory Schedule and Deadlines (2026)

This investigation represents a "second front" in the regulatory landscape. While the BIOSECURE Act focuses on national security and data privacy, Inv. No. 332-610 focuses on economic nationalism and fair competition. For companies engaged in cross-border licensing, this means that even if an asset is secure from a data perspective, its valuation could be impacted by future trade measures addressing price distortions and state-subsidized overcapacity.

FDA Oncology Center of Excellence and Global Clinical Harmonization

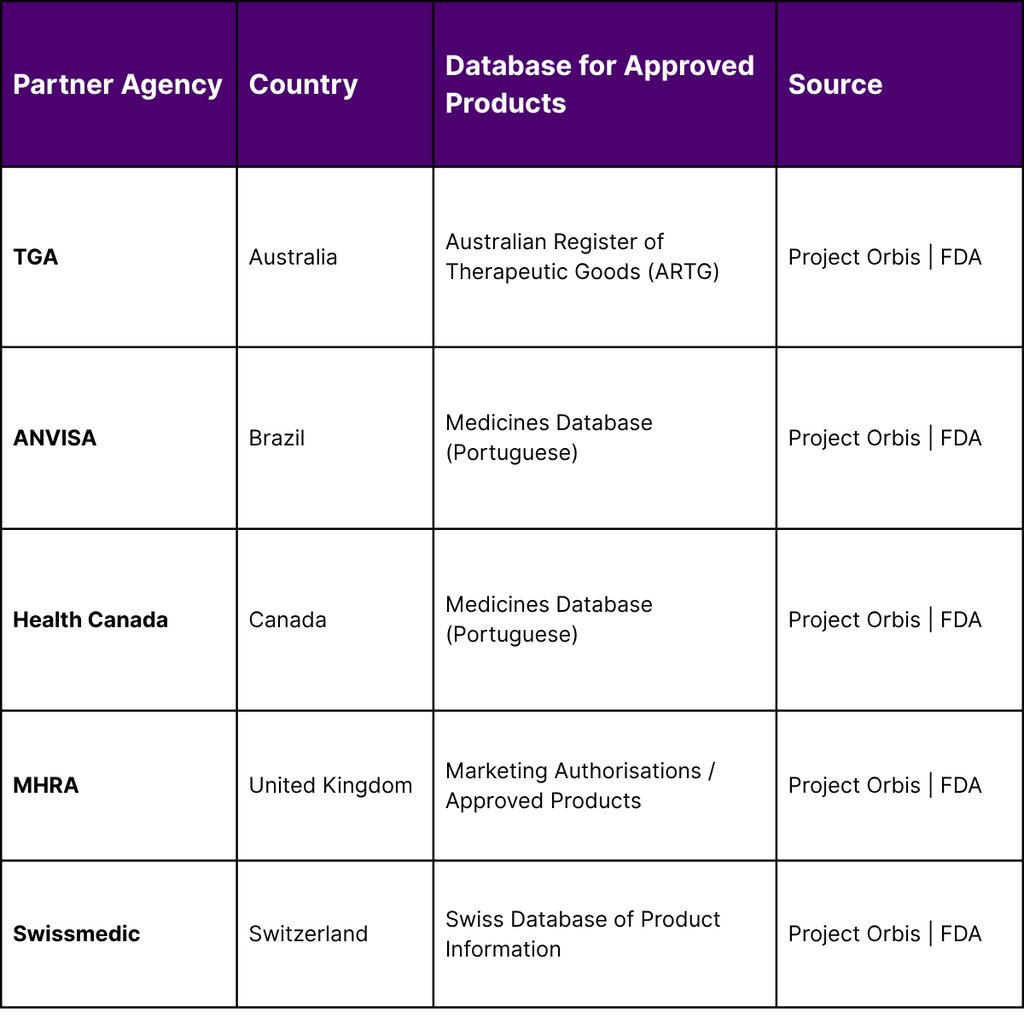

Despite the increasing geopolitical friction, regulatory collaboration in oncology continues to provide a vital pathway for Asian assets to enter the U.S. market. The FDA’s Oncology Center of Excellence (OCE), authorized by the 21st Century Cures Act, leads several initiatives to advance global drug development. The most prominent of these is Project Orbis, a framework that allows for the concurrent submission and review of oncology products among international partners.

As of January 26, 2026, Project Orbis includes a coalition of regulators from Australia, Brazil, Canada, Israel, Singapore, Switzerland, and the United Kingdom. This collaborative review process is essential for the Asia-U.S. corridor because pivotal clinical trials in oncology are increasingly conducted internationally. By establishing greater uniformity in global standards of treatment, Project Orbis ensures that a drug approved in one jurisdiction can more easily navigate the regulatory hurdles of another.

Integration of International Oncology Assets (January 2026 Update)

The OCE quarterly reports provide a window into the Adoption of new therapies. In the fourth annual Oncology News Central (ONC) Drug Report, covering late 2024 to late 2025, nearly 9 in 10 oncology clinicians reported prescribing new drugs or existing drugs for new indications a statistically significant increase from previous years. However, this adoption is increasingly tempered by cost pressures and prior authorization barriers, which continue to influence prescribing decisions for 75% of clinicians.

The OCE’s specialized programs, such as the Immuno-Oncology Program and the Precision Oncology Program, are specifically designed to evaluate the types of advanced assets coming out of China and South Korea. Projects like "Project Optimus" and "Project FrontRunner" are currently working to reform dose optimization and advance therapies into the early clinical setting, respectively efforts that are critical for the survival of early-stage Asian biotechs looking for Western partners.

Strategic Analysis of Corporate Pipelines and Financial Resilience

The financial health of companies within the biotech corridor in early 2026 is varied, with some firms struggling to maintain liquidity while others leverage massive balance sheets for strategic acquisitions. HCW Biologics, for example, reported "substantial doubt" about its ability to continue as a going concern in March 2026, yet it still successfully licensed a preclinical molecule (HCW11-006) for a $3.5 million upfront fee and double-digit royalties. This illustrates that even distressed firms can find value in the current licensing surge.

In contrast, industry giants like Pfizer have reaffirmed their 2026 financial guidance with revenues expected in the range of $59.5 billion to $62.5 billion. Pfizer's strategy includes the start of approximately 20 key pivotal trials in 2026, supported by assets acquired through licensing deals with firms like 3SBio and YaoPharma in the oncology and cardiometabolic sectors. Similarly, Merck continues to manage significantly lower sales of some core products in China (such as Gardasil), which has intensified its focus on in-licensing new Phase 3 oncology candidates to diversify its revenue streams.

Key Q1 2026 Licensing and Pipeline Financials

The financial narrative of 2026 is one of consolidation. Large-cap pharma companies are using their cash reserves to acquire "de-risked" assets from Asian innovators, while small-cap biotechs are using these licensing fees as a lifeline to survive Nasdaq compliance notices and clinical trial expenses.

Conclusion: The Future of the Asia-U.S. Biotech Axis

The $60 billion surge in oncology licensing during the first quarter of 2026 marks a definitive shift in the global biopharmaceutical market. Western pharmaceutical companies, facing a catastrophic "patent cliff," have recognized that their future survival depends on integrating the high-quality, high-velocity innovation emerging from China and South Korea. This corridor, however, is no longer just a conduit for capital and molecules; it is a high-stakes geopolitical battleground.

To succeed in this environment, firms must adopt a dual-strategy approach. On one hand, they must continue to aggressively source the "best-in-class" therapies that the Asian "Biotech 2.0" era is producing. On the other, they must build resilient, compliant supply chains that can withstand the scrutiny of the BIOSECURE Act and the USITC’s investigations into state support and pricing practices. The transition period provided by the law offers a window for strategic pivot, but the market behavior in early 2026 suggests that the winners will be those who move faster than the regulatory deadlines.

The convergence of global clinical collaboration through Project Orbis and the economic pressures of revenue erosion has created a permanent dependency on cross-border innovation. The Asia-U.S. biotech corridor, despite its hurdles, remains the most vital artery for the future of global oncology.

Frequently Asked Questions (FAQ)

1. What is the "Patent Cliff" mentioned in the report?

The patent cliff refers to the period between 2025 and 2030 when 190 drugs, including 69 blockbusters, will lose patent protection. GlobalData estimates this will cause a $230 billion drop in U.S. drug sales, forcing companies to find new assets through licensing.

2. Which Chinese companies are considered "Biotechnology Companies of Concern"?

While the Office of Management and Budget (OMB) is still finalizing the list, companies already on the Department of Defense's 1260H list, such as WuXi AppTec, are widely cited as primary targets of the BIOSECURE Act.

3. What is the timeline for the BIOSECURE Act restrictions?

Restrictions for companies on the 1260H list can take effect as early as 2026 (60 days after the Federal Acquisition Regulation is updated). For other designated "Companies of Concern," there is generally a five-year transition period for existing contracts.

4. How does USITC Investigation No. 332-610 differ from the BIOSECURE Act? The BIOSECURE Act focuses on national security and data privacy, whereas the USITC investigation focuses on the economic impact of Chinese state subsidies and pricing practices on U.S. industry competitiveness.

5. Is Project Orbis still reviewing oncology assets from China and South Korea?

Yes. Project Orbis facilitates the concurrent review of oncology products across multiple countries. The FDA continues to use this framework to ensure that clinical trials conducted internationally meet U.S. standards for safety and efficacy.

References

Bureau of Economic Analysis. (2026, March). U.S. International Trade in Goods and Services, January 2026. U.S. Department of Commerce.

Federal Register. (2026, March 2). Impact on U.S. Industry of China's State Support and Pricing Practices in the Biotechnology Sector (Investigation No. 332-610). 91 FR 10153.

Food and Drug Administration. (2026, January 26). Project Orbis Approvals. Oncology Center of Excellence.

U.S. Census Bureau. (2026, March). Monthly U.S. International Trade in Goods and Services, January 2026 (FT900).

U.S. Chamber of Commerce. (2026). 2026 International IP Index: Executive Summary.

U.S. International Trade Commission. (2026, February 26). USITC to Investigate State Support and Pricing Practices by Chinese Biotechnology Firms. News Release 26-030.

U.S. Securities and Exchange Commission. (2026, March 31). HCW Biologics Inc. Form 8-K: Results of Operations and Financial Condition.

U.S. Securities and Exchange Commission. (2026, February 19). Vir Biotechnology, Inc. Form 8-K: Entry into a Material Definitive Agreement.

U.S. Securities and Exchange Commission. (2026, January 23). Pfizer Inc. Form 8-K: 2026 Financial Guidance.

Navigation

© 2026 FyreIgnis Market Research. All rights reserved.

Legal

info@fyreignismarketresearch.com

India