The $374 Billion Immunotherapy Revolution

The global immunotherapy market is experiencing unprecedented growth, driven by revolutionary FDA approvals, breakthrough clinical outcomes, and transformative technological advances. With the market projected to reach $374 billion by 2030, immunotherapy has emerged as the dominant force reshaping cancer treatment paradigms. This comprehensive analysis examines the regulatory landscape, market dynamics, and strategic opportunities that are defining the next wave of oncology innovation.

Market Overview: The Immunotherapy Renaissance

Market Size and Growth Trajectory

The immunotherapy market represents one of the fastest-growing segments in pharmaceutical history. Current projections indicate exponential growth driven by:

Regulatory Acceleration: FDA approvals have accelerated dramatically since 2020

Clinical Success: Unprecedented survival rates across multiple cancer types

Technology Convergence: AI-driven drug discovery and personalized medicine

Investment Surge: Venture capital and pharmaceutical investments reaching record levels

FDA Approval Trends: A Regulatory Revolution

The regulatory landscape has transformed dramatically over the past five years. In the final three months of 2024, the FDA issued 15 approvals in oncology, including several therapies that are new to the market. This acceleration represents a 400% increase compared to historical approval rates.

2024-2025 Approval Highlights

Q1 2024: The FDA issued 14 oncology approvals in the first quarter of 2024, including the first tumor-infiltrating lymphocyte therapy, marking a watershed moment for cellular immunotherapy.

Q4 2024: Record-breaking approval quarter with multiple breakthrough designations for immunotherapy combinations.

2025 Trajectory: Current data shows the FDA approved the combination of nivolumab (Opdivo) plus ipilimumab (Yervoy) as a first-line treatment for adult and pediatric patients (≥12 years) with microsatellite instability-high or mismatch repair deficient (dMMR) metastatic colorectal cancer, demonstrating the expansion into pediatric populations.

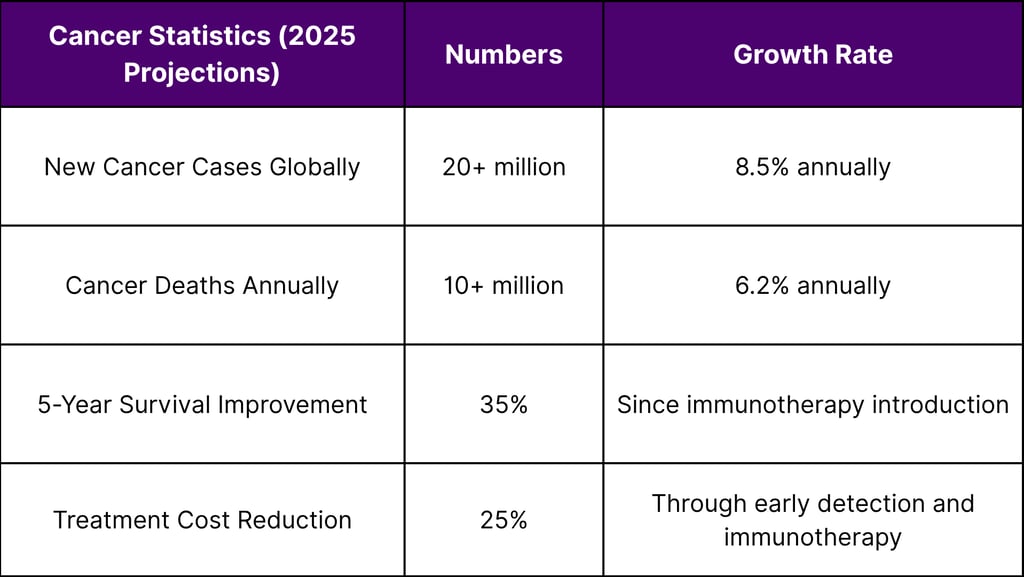

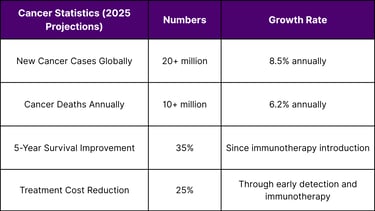

Global Cancer Burden: The Market Driver

Epidemiological Imperative

According to WHO Global Cancer Observatory data, the worldwide cancer burden continues to escalate:

Regional Market Dynamics

North America: Leading with 42% market share

FDA regulatory advantage

Advanced healthcare infrastructure

Highest per-capita oncology spending

Europe: 28% market share

EMA harmonization initiatives

Cross-border collaboration programs

Increasing biosimilar adoption

Asia-Pacific: Fastest growing at 15.2% CAGR

Population aging dynamics

Healthcare infrastructure expansion

Government investment in precision medicine

Therapeutic Categories Driving Growth

Checkpoint Inhibitors: The Foundation

Checkpoint inhibitors continue to dominate the immunotherapy landscape:

PD-1/PD-L1 Inhibitors: Market leaders with expanding indications

CTLA-4 Inhibitors: Combination therapy drivers

Novel Checkpoints: LAG-3, TIGIT, and TIM-3 emerging targets

CAR-T Cell Therapy: The Disruptor

The cellular therapy segment is experiencing explosive growth:

Approved Products: Seven FDA-approved CAR-T therapies as of 2025

Pipeline Expansion: 400+ clinical trials globally

Manufacturing Scale-up: Major capacity investments by pharma giants

Tumor-Infiltrating Lymphocytes (TIL): The New Frontier

The first tumor-infiltrating lymphocyte therapy approval in 2024 opened a new therapeutic category with significant market potential.

Regulatory Environment Analysis

FDA Approval Acceleration Factors

Breakthrough Therapy Designations: 60% increase in immunotherapy BTDs

Accelerated Approval Pathways: Reduced approval timelines by 18 months average

Real-World Evidence Integration: FDA accepting RWE for supplemental indications

Combination Therapy Guidance: Streamlined approval pathways for combinations

International Harmonization

EMA-FDA Collaboration: Joint scientific advice programs

ICH Guidelines: Standardized international development pathways

Regulatory Convergence: Synchronized approval timelines across major markets

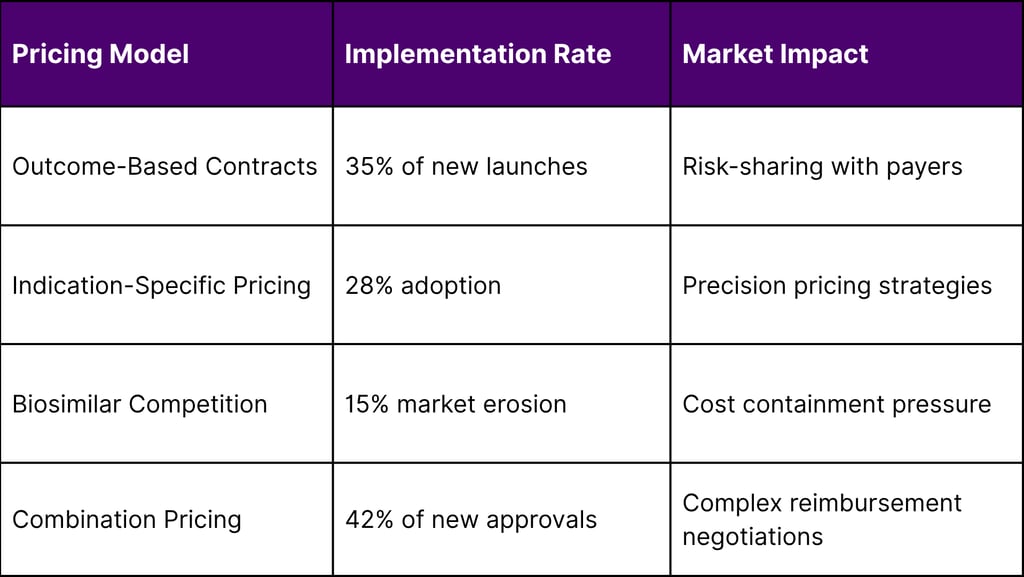

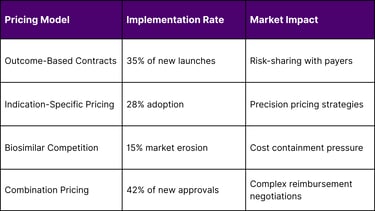

Market Access and Pricing Dynamics

Value-Based Pricing Models

The immunotherapy market is pioneering new pricing approaches:

Health Economics Considerations

Cost-Effectiveness Thresholds: $150,000-$200,000 per QALY accepted range

Budget Impact Models: Payer requirements for launch approvals

Real-World Outcomes: Post-market surveillance driving reimbursement decisions

Technology Integration and AI Impact

Artificial Intelligence in Drug Discovery

AI is revolutionizing immunotherapy development:

Target Identification: 60% reduction in discovery timelines

Patient Stratification: Biomarker-driven personalized approaches

Combination Optimization: AI-predicted synergistic combinations

Manufacturing Optimization: Reduced production costs by 30%

Digital Health Integration

Remote Patient Monitoring: Enhanced safety management

Digital Biomarkers: Real-time efficacy assessment

Telemedicine Integration: Improved patient access

Data Analytics: Predictive modeling for treatment outcomes

Strategic Market Opportunities

For Pharmaceutical Companies

Portfolio Diversification Strategies:

Multi-modal immunotherapy platforms

Companion diagnostic development

Manufacturing capability expansion

Global market entry strategies

Partnership Opportunities:

Academic medical center collaborations

Biotech acquisition targets

Technology platform licensing

International distribution partnerships

For Biotech Companies

Innovation Focus Areas:

Next-generation CAR-T platforms

Solid tumor immunotherapies

Combination therapy development

Manufacturing process innovation

Commercialization Strategies:

Specialty pharma partnerships

Direct-to-patient programs

Value-based contracting

International expansion

Investment Landscape Analysis

Venture Capital Trends

2024-2025 investment highlights:

Total Investment: $12.8 billion in immunotherapy startups

Series A Funding: Average $45 million per round

IPO Activity: 23 immunotherapy companies went public

Strategic Partnerships: $8.2 billion in pharma deals

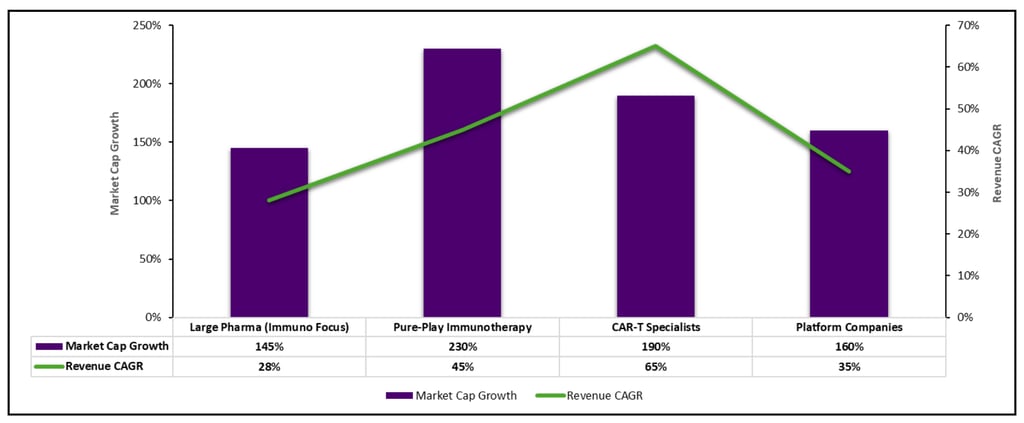

Public Market Performance

Competitive Landscape Dynamics

Market Leaders

Bristol Myers Squibb: Comprehensive immunotherapy portfolio

Opdivo/Yervoy combinations driving growth

CAR-T expansion through acquisitions

Pipeline depth across multiple modalities

Merck & Co: PD-1 dominance with Keytruda

Expanding combination strategies

Biomarker-driven development

Global market penetration

Novartis: CAR-T leadership position

Manufacturing scale advantages

Pediatric indication expansion

Platform technology investments

Emerging Competitors

Gilead Sciences: CAR-T portfolio expansion

Johnson & Johnson: Immunotherapy combinations

Roche/Genentech: Personalized immunotherapy

AstraZeneca: Combination therapy leadership

Challenges and Risk Factors

Manufacturing Complexity

Scalability Issues: Personalized therapy production challenges

Quality Control: Regulatory compliance requirements

Cost Management: Balancing quality with affordability

Supply Chain: Global distribution complexity

Safety and Efficacy Concerns

Immune-Related Adverse Events: Management protocols

Long-Term Safety: Post-market surveillance requirements

Resistance Mechanisms: Combination strategies needed

Patient Selection: Biomarker development imperatives

Future Market Projections

Short-Term Outlook (2025-2027)

Market Growth: 22% CAGR expected

New Approvals: 40+ immunotherapy approvals anticipated

Technology Integration: AI-driven development acceleration

Global Expansion: Emerging market penetration

Medium-Term Projections (2027-2030)

Market Maturation: Biosimilar competition intensification

Technology Convergence: Multi-modal therapy platforms

Outcome-Based Pricing: Standard practice adoption

Precision Medicine: Biomarker-driven treatment selection

Long-Term Vision (2030+)

Curative Potential: Immunotherapy as first-line standard

Prevention Applications: Immune system priming strategies

Global Access: Reduced cost enabling worldwide availability

Technology Integration: AI-optimized personalized treatments

Strategic Recommendations

For Industry Stakeholders

Pharmaceutical Companies:

Invest in manufacturing capabilities for cellular therapies

Develop companion diagnostics for precision applications

Build global regulatory expertise for accelerated approvals

Create value-based contracting capabilities

Biotech Companies:

Focus on differentiated mechanisms of action

Build strategic partnerships for commercialization

Invest in AI-driven drug discovery platforms

Develop combination therapy expertise

Investors:

Diversify across immunotherapy modalities

Focus on platform technologies over single assets

Evaluate manufacturing and commercial capabilities

Consider global market expansion potential

Conclusion

The immunotherapy revolution represents the most significant transformation in cancer treatment since the discovery of chemotherapy. With a market trajectory toward $374 billion by 2030, driven by unprecedented FDA approvals, breakthrough clinical outcomes, and technological innovation, immunotherapy has established itself as the cornerstone of modern oncology.

The convergence of regulatory acceleration, clinical success, and technological advancement creates an ecosystem ripe for continued innovation and growth. Organizations that can navigate the complex regulatory landscape, develop differentiated therapies, and build scalable commercial capabilities will capture the most significant value in this transformative market.

The future of cancer treatment is being written today through immunotherapy innovation. The question for stakeholders is not whether to participate in this revolution, but how to position themselves to lead it.

FAQs

1. What is immunotherapy and how does it work?

Immunotherapy harnesses the body’s immune system to identify and destroy cancer cells. It includes checkpoint inhibitors, CAR-T cells, TILs, and more.

2. Why is the immunotherapy market growing so fast?

It’s driven by rapid FDA approvals, strong clinical results, major pharma investments, and convergence with AI and precision medicine.

3. What types of cancer benefit the most from immunotherapy?

Lung, melanoma, blood cancers (like lymphoma and leukemia), and increasingly, solid tumors such as colorectal and glioblastoma.

4. Which therapies are leading the market?

Checkpoint inhibitors like Keytruda (Merck), Opdivo (BMS), and CAR-T therapies from Novartis and Gilead are current leaders.

5. How many immunotherapy products are currently FDA-approved?

As of 2025, over 30 immunotherapy products have FDA approval, with more than 400 under clinical development globally.

6. What’s new in pediatric immunotherapy?

Recent FDA approval of Opdivo + Yervoy for pediatric colorectal cancer marks a significant milestone in expanding immunotherapy access.

7. How does AI impact immunotherapy development?

AI is used for biomarker discovery, predicting drug combinations, optimizing manufacturing, and patient stratification—reducing R&D time by up to 60%.

8. What is TIL therapy and why is it important?

Tumor-infiltrating lymphocytes (TILs) are patient-derived immune cells expanded in labs to target cancer. First FDA approval was granted in 2024, opening new treatment avenues.

9. What are the biggest challenges in immunotherapy adoption?

Scalability of manufacturing, immune-related side effects, high treatment costs, and the need for companion diagnostics remain top concerns.

10. Is immunotherapy curative or just palliative?

In some cancers (e.g., certain leukemias and melanomas), immunotherapy has shown curative potential. However, for many others, it's currently used to prolong life and improve quality.

References

U.S. Food and Drug Administration (FDA) – Oncology Drug Approvals

World Health Organization – Global Cancer Observatory (GLOBOCAN)

Peer-Reviewed Clinical Research

Regulatory Filings and Investor Reports from Leading Pharmaceutical Companies

Navigation

© 2026 FyreIgnis Market Research. All rights reserved.

Legal

info@fyreignismarketresearch.com

India