The Impact of the Inflation Reduction Act (IRA) on Oncology R&D Portfolios

The global pharmaceutical industry is navigating a transformative epoch defined by the implementation of the Inflation Reduction Act (IRA) of 2022. As of April 2026, the initial theoretical concerns regarding the legislation have crystallized into measurable strategic shifts within the research and development (R&D) portfolios of the world’s leading oncology firms. The core mechanism driving this change is the Medicare Drug Price Negotiation Program (DPNP), which has introduced a fundamental economic bifurcation between small-molecule drugs and large-molecule biologics. This report analyzes how these price negotiations are forcing biopharmaceutical companies to rethink their fundamental development strategies, specifically focusing on the "pill penalty" and the subsequent realignment of oncology pipelines.

The Economic Architecture of the Inflation Reduction Act

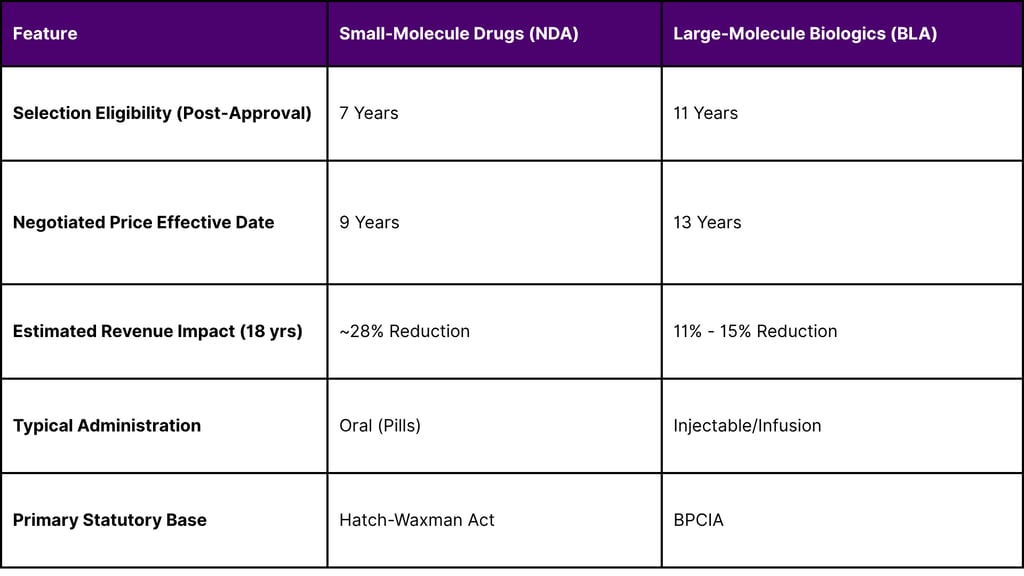

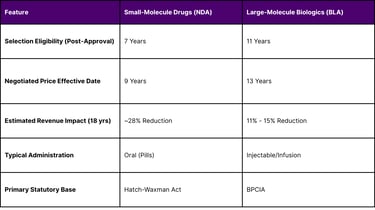

The Inflation Reduction Act grants the U.S. federal government, through the Centers for Medicare & Medicaid Services (CMS), the authority to set a “Maximum Fair Price” (MFP) for the highest-spending drugs in the Medicare program. The implementation of these prices follows a schedule that differentiates between molecular types, creating a significant disparity in the "negotiation-free" period available to innovators.

The 9-Year vs. 13-Year Negotiation Timeline

Under the current statutory framework, small-molecule drugs, typically approved under a New Drug Application (NDA), become eligible for selection for price negotiation seven years after FDA approval. The resulting MFP takes effect two years later, effectively capping the period of market-based pricing at nine years. In contrast, large-molecule biologics, approved under a Biologics License Application (BLA), are eligible for selection 11 years post-approval, with the MFP taking effect at year 13.

This four-year gap represents a significant portion of a drug’s most profitable lifecycle phase. Historically, many blockbuster oncology treatments achieved their peak annual global revenue around year 11 or 12. By subjecting small molecules to price controls in year 9, the IRA truncates this peak revenue window. Economic modeling suggests that revenue from small-molecule drugs subject to an MFP could be reduced by approximately 28% over an 18-year period. Biologics, benefiting from an additional four years of market exclusivity, face a comparatively lower revenue reduction of 11% to 15%.

Table 1: Comparative Statutory Timelines for Medicare Price Negotiation

The divergence in these timelines has introduced a "pill penalty" that disincentivizes the development of oral therapies, which are often preferred by patients for their convenience and lower administration costs. For oncology-focused firms, this penalty is particularly acute given that kinase inhibitors and other small-molecule targeted therapies are cornerstones of modern cancer care.

Oncology as the Epicenter of DPNP Implementation

Oncology remains the primary therapeutic focus for the pharmaceutical industry, accounting for roughly 16% of total global spending and 30% of all compounds in development. However, the high cost and high utilization of cancer drugs within the Medicare population have made them primary targets for the initial cycles of price negotiation.

Analysis of Negotiation Cycles (2026–2028)

As of April 2026, CMS has concluded the first two rounds of negotiation and is currently engaged in the third cycle. The first cycle, with prices effective January 1, 2026, included Imbruvica (ibrutinib), a small-molecule kinase inhibitor used for leukemia and lymphoma. The second cycle, with prices effective in 2027, expanded to include four additional cancer treatments: Xtandi, Pomalyst, Ibrance, and Calquence.

In January 2026, CMS announced the 15 drugs selected for the third cycle of negotiations, with MFPs taking effect in 2028. This list features high-expenditure oncology treatments that have transitioned into the 7-year selection window.

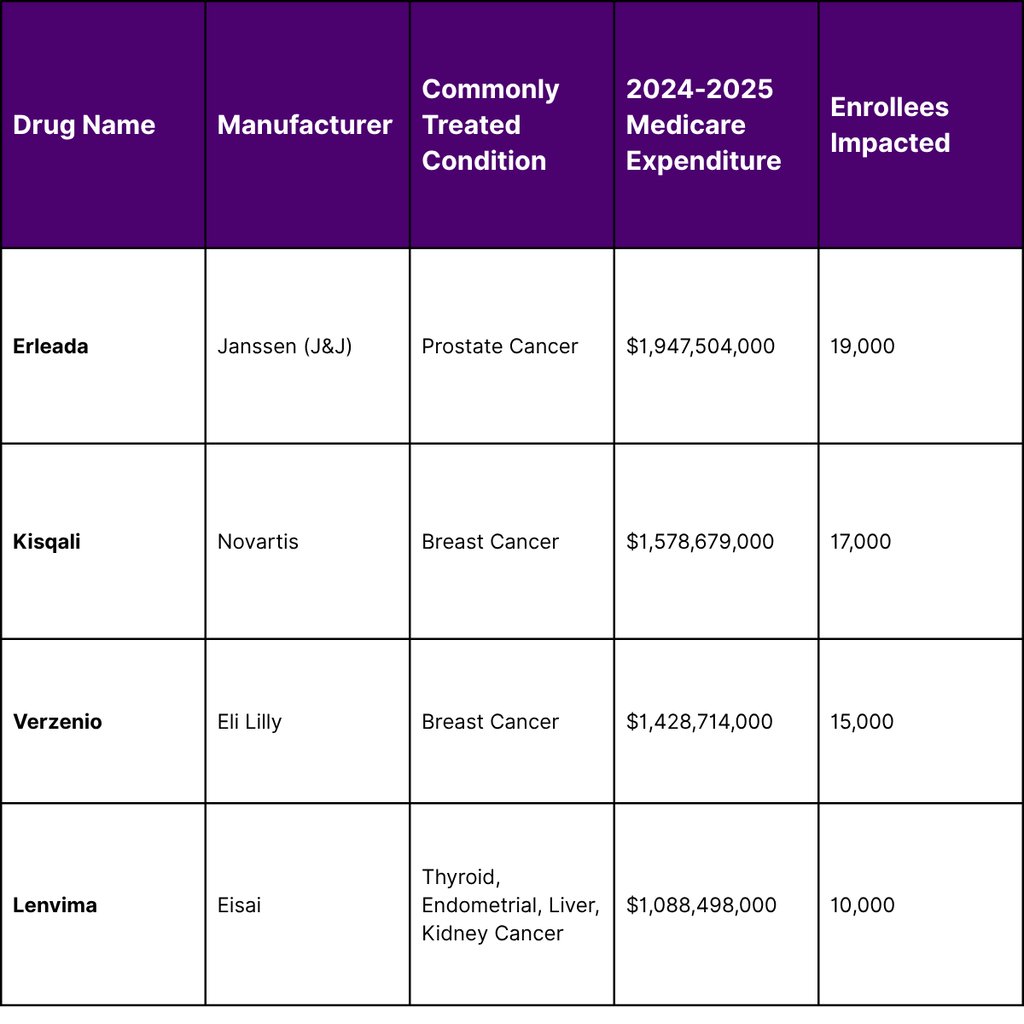

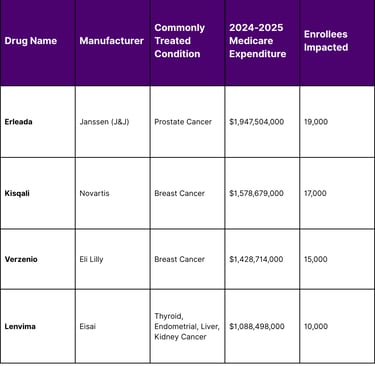

Table 2: Oncology Drugs Selected for 2028 Medicare Price Negotiation

These four oncology drugs alone accounted for approximately $6.04 billion in Medicare spending between November 2024 and October 2025. The inclusion of these therapies underscores the systematic targeting of small-molecule oncology blockbusters. Manufacturers of these products are now forced to operate under a pricing environment where government-negotiated rates replace market-driven list prices and rebates.

The Strategic Pivot: Rethinking "Small vs. Large" Molecules

The 9-year vs. 13-year disparity has triggered a significant reallocation of capital within R&D portfolios. Strategic market intelligence from firms like FyreIgnis Market Research suggests that biotech disruptors and pharma trailblazers are increasingly prioritizing biologic platforms over small-molecule projects to preserve long-term commercial value.

Decline in Small-Molecule Investment

Since the legislative framework of the IRA was first proposed in late 2021, funding for small-molecule drug development has reportedly declined by 70%. Venture capital firms have also signaled a retreat; surveys indicate that 76% of VC firms plan to divest from small-molecule projects, and 87% believe the IRA will decrease overall interest in this modality.

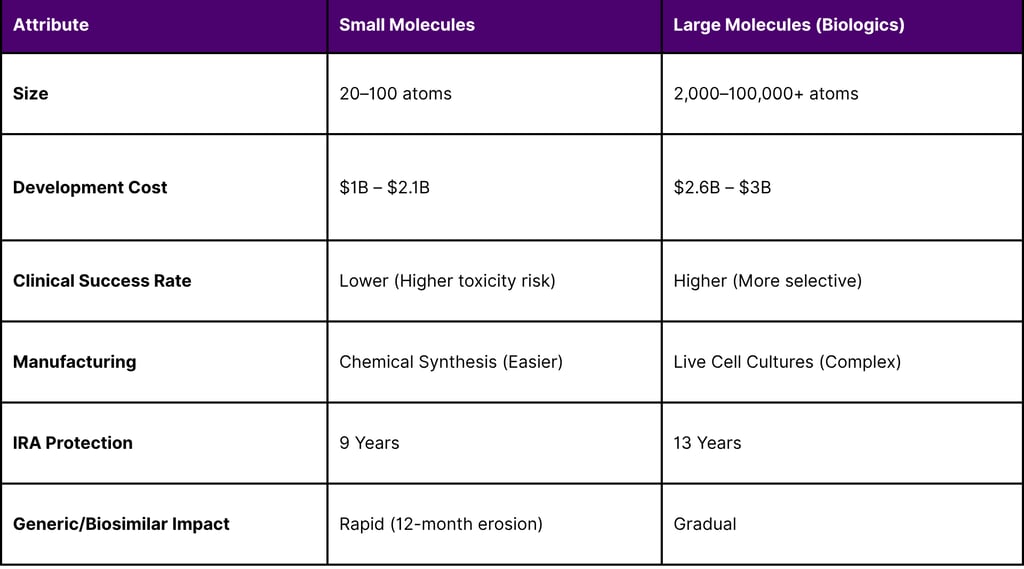

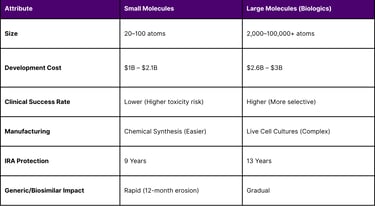

The physical and chemical differences between these molecules further drive this shift. Small molecules, composed of 20 to 100 atoms, are susceptible to rapid generic competition once exclusivity ends. Biologics, which can be 1,000 times larger and are produced from living organisms, have a more resilient "moat" due to manufacturing complexity and the slower market uptake of biosimilars.

Table 3: Molecular Characteristics and Investment Risk Profiling

Case Study: The "Pill Penalty" in Ovarian Cancer

The approval of Lifyorli (relacorilant) in March 2026 for platinum-resistant ovarian cancer illustrates the ongoing clinical necessity of small molecules. Despite its high clinical value, its status as a small molecule places it on a 9-year negotiation clock. In contrast, biologic checkpoint inhibitors like pembrolizumab (Keytruda) or nivolumab (Opdivo), which are also used extensively in oncology, enjoy the full 13-year window. This economic reality is forcing firms to ask whether a new oncology target should be pursued with a small-molecule inhibitor or a more complex antibody-drug conjugate (ADC), even if the small molecule offers better patient convenience.

Impact on Post-Approval Clinical Development

A critical, often overlooked consequence of the IRA is its impact on "secondary indications." In oncology, a drug is frequently launched for a narrow, late-stage indication and subsequently studied for earlier lines of therapy or adjuvant settings.

The Disincentive for Lifecycle Expansion

Because the 7-year selection clock starts at the date of the drug’s initial FDA approval, any subsequent approvals for new cancer types do not reset the timer. Consequently, if a drug is approved for a small orphan population in year 1 and a massive blockbuster indication in year 6, it may still be selected for negotiation in year 7 based on the combined Medicare spend.

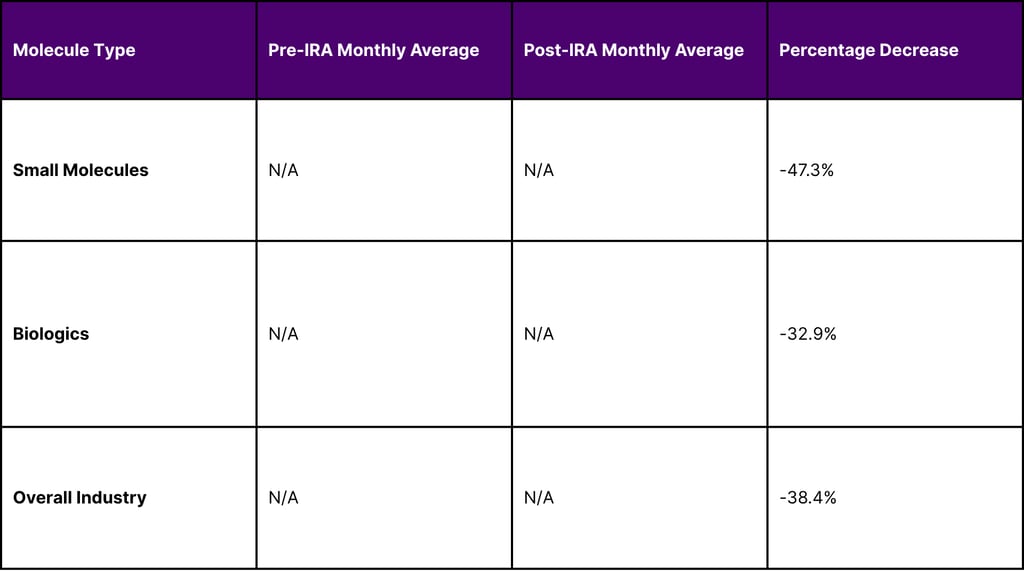

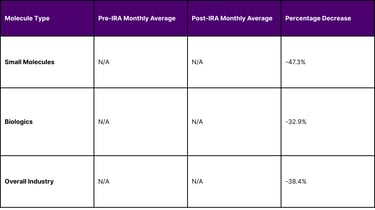

This has led to a documented decline in industry-funded post-approval trials. A difference-in-difference analysis of oncology trials initiated between 2014 and 2024 found that post-approval trial initiations for small molecules fell by an additional 4.5 trials per month compared to biologics after the passage of the IRA. Overall, industry-sponsored trials on previously approved drugs decreased by 38.4%.

Table 4: Post-IRA Decline in Industry-Sponsored Phase I-III Trials

This trend suggests that manufacturers are opting for "one-and-done" launch strategies or delaying initial launches until larger indications are ready, thereby depriving patients of early access to treatments for rare cancers.

Fiscal Turmoil in Medicare Part D (2026–2027)

As of April 2026, the Medicare Part D program is experiencing unprecedented volatility. While the IRA’s price negotiations were intended to lower government spending, the total Part D budget is projected to increase significantly due to benefit redesign and shifting insurer behaviors.

The 35% Surge in Part D Bids

In late 2025 and early 2026, the CBO identified a massive discrepancy between previous projections and actual insurer bids for the 2026 plan year. Bids from private insurance plans anticipated a 35% increase in annual per-enrollee costs, a figure that dwarfs the historical average growth of less than 6%.

Several drivers contribute to this surge:

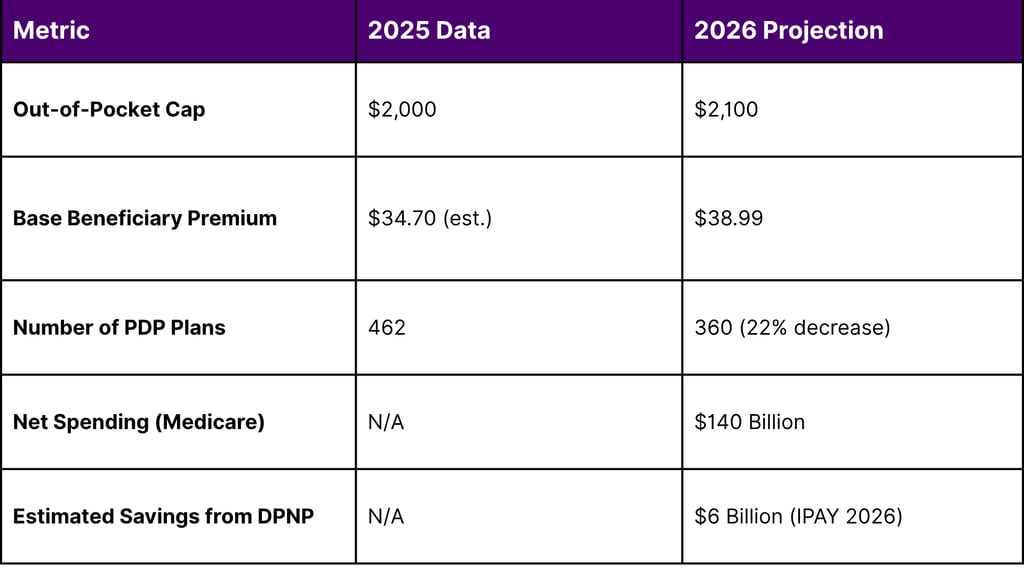

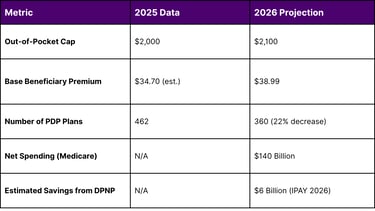

Redesign of Catastrophic Coverage: The IRA capped beneficiary out-of-pocket spending at $2,100 in 2026 and eliminated the 5% coinsurance requirement, shifting massive liability from seniors to insurers and the government.

Increased Utilization: Lower out-of-pocket costs have encouraged higher use of specialty drugs, particularly in oncology and immunology.

Insurer Overhead: CMS revised its estimate of insurers' overhead costs for 2026 from 6.5% to 11.4% to account for market instability and new cost-sharing limits.

Table 5: Key Medicare Part D Cost and Enrollment Projections for 2026

The CBO warns that if these costs remain elevated, Medicare spending on Part D could be $500 billion higher over the next decade than originally projected. This suggests that the "savings" from price negotiations are being rapidly offset by the increased costs of the Part D benefit redesign.

Clinician Perspectives and Access Barriers

The impact of the IRA extends beyond the corporate boardroom into the oncology clinic. The 2026 Oncology News Central (ONC) Drug Report, which surveyed nearly 300 clinicians, provides a "boots-on-the-ground" view of these changes.

Prescribing Patterns and Prior Authorization

Nearly 90% of oncology clinicians reported prescribing new drugs or indications in the past year, but their habits are becoming more selective. The proportion of clinicians frequently prescribing a new drug fell from 44% in 2024 to 35% in 2025.26 Cost and insurance reimbursement issues remain a primary hamper for 75% of clinicians.

Furthermore, the rise of Pharmacy Benefit Manager (PBM) influence is causing frustration. Clinicians cite "PBM greed" and "interference" as top concerns that delay patient access to newly approved therapies. Interestingly, while some clinicians have become more adept at navigating prior authorization, 18% reported frequently avoiding prescribing new drugs specifically to avoid the administrative burden.

Adoption of Biosimilars in Oncology

While small molecules face the "pill penalty," biologics are navigating a maturing biosimilar market. In oncology, physician confidence in biosimilars is high, with 99% of practices reporting they are confident in explaining these products to patients. This is critical as major oncology biologics like Keytruda, Opdivo, and Perjeta face exclusivity losses before 2030.

However, the "Stelara Paradox" of 2026 highlights a new policy challenge: the collision of Medicare negotiation and biosimilar competition. In early 2026, the negotiated MFP for Stelara took effect at a ~66% discount, even as biosimilar competition had already driven market prices down by 85–90%. This creates a situation where the government-negotiated price may actually be higher than the market price for biosimilars, potentially distorting competition and discouraging new biosimilar entrants.

Strategic Portfolio Adjustments in 2026

To mitigate the risks of the IRA, oncology firms are adopting a new set of strategic pillars. These strategies are designed to maximize the 13-year biologic window and protect the value of innovative assets.

1. Modality Shifting and Platform Innovation

Firms are increasingly moving away from "naked" small-molecule inhibitors toward biologics-based platforms. Antibody-drug conjugates (ADCs) are a prime example. By using a biologic antibody to deliver a small-molecule toxin, manufacturers can qualify the entire product for the 13-year biologic clock while maintaining the potency of chemical cell-killing agents.

2. Strategic Indication Sequencing

The "orphan first" strategy is being replaced by a "blockbuster first" or "simultaneous launch" strategy. If a drug is approved for a large indication initially, it captures more value before the 9-year or 13-year clock runs out. Launching for a small orphan indication first is now viewed as an "economic liability" that prematurely starts the negotiation timer.

3. Leveraging the Orphan Drug Exclusion

The IRA exempts drugs with a single orphan indication from negotiation. This has led to a surge in R&D for "ultra-rare" conditions where the drug is unlikely to ever seek a second indication. However, for most oncology drugs, this is a restrictive strategy that limits the total addressable market.

4. Manufacturing as a Defense

Biologic manufacturing complexity is being used as a strategic moat. Because biosimilars are harder to produce than generics, the revenue erosion after year 13 is expected to be more gradual than the "patent cliff" seen in small molecules.

Recent Regulatory and Funding Milestones (April 2026)

The regulatory landscape in April 2026 continues to evolve in response to both the IRA and broader technological trends like AI in drug discovery.

FDA Approvals in Q1 2026

The first quarter of 2026 saw nine landmark approvals in oncology. These approvals reflect a move toward biomarker-driven therapies and combination regimens that include both small and large molecules.

Lifyorli (relacorilant): Approved March 25, 2026, for platinum-resistant ovarian cancer. A notable small-molecule win, yet vulnerable to the IRA timeline.

Nivolumab (Opdivo) + Chemotherapy: Approved March 20, 2026, for untreated advanced classical Hodgkin lymphoma, changing the frontline standard.

Teclistamab (Tecvayli) + Daratumumab: Approved March 5, 2026, for relapsed multiple myeloma. A complex bispecific/monoclonal combination.

Zongertinib (Hernexeos): Granted accelerated approval on February 26, 2026, for HER2-mutant non-small cell lung cancer.

Federal Funding for Oncology Research

In early 2026, Congress passed the Consolidated Appropriations Act of 2026, providing a "meaningful boost" to federal research. The NIH budget rose to $47.2 billion, with the NCI receiving $7.35 billion a $128 million increase over 2025. This funding is crucial for maintaining the basic science pipeline, although the administration has proposed capping indirect cost reimbursements at 15%, a move strongly opposed by the research community as a threat to high-level clinical trials.

The Road Ahead: Legislative and Market Outlook

The "pill penalty" remains a point of intense advocacy. The Ensuring Pathways to Innovative Cures (EPIC) Act, introduced in 2025 and 2026, seeks to equalize the negotiation period for small molecules at 13 years. Proponents argue this is necessary to ensure that oral cancer medications and neurological treatments which are predominantly small molecules remain viable for development.

Furthermore, the "GLOBE" model proposed by CMS in late 2025 seeks to implement international price referencing, which could further lower the prices Medicare pays for drugs. This move is being met with significant resistance from the Biotechnology Innovation Organization (BIO) and other industry leaders who argue it will further erode the foundations of U.S. biopharmaceutical leadership.

Conclusion

As of April 2026, the Inflation Reduction Act has fundamentally altered the calculus of oncology drug development. The "pill penalty" is not merely a pricing challenge but a strategic force that is actively shifting the industry toward biologics, ADCs, and bispecific therapies. While Medicare beneficiaries are beginning to see the benefits of negotiated prices and out-of-pocket caps, the long-term impact on oncology innovation particularly in the realm of oral therapies and secondary indications is only beginning to be quantified.

For firms like FyreIgnis Market Research, the mission is to provide the strategic clarity needed to navigate this complex environment.12 Leaders in the oncology space must balance the clinical needs of patients with the economic realities of a government-regulated market. Success in the post-IRA era will be defined by those who can successfully navigate the molecular divide and leverage the 13-year biologic moat while continuing to deliver life-saving innovations to the bedside.

FAQ

What exactly is the "pill penalty" under the Inflation Reduction Act?

The "pill penalty" refers to the statutory difference in when Medicare can begin price negotiations. Small-molecule drugs (pills) can be selected for negotiation 7 years post-approval, with prices effective in year 9. Large-molecule biologics are not eligible until year 11, with prices effective in year 13.

How has the IRA affected the development of new cancer indications for existing drugs?

Because the 7-year selection "clock" begins at the date of the first approval and does not reset for new indications, manufacturers are disincentivized from pursuing follow-on approvals for rare cancers or earlier lines of therapy. This has contributed to a 38.4% decline in post-approval industry-sponsored trials.

Which oncology drugs are subject to the 2028 negotiated prices?

The 2028 cycle includes Erleada (prostate cancer), Kisqali (breast cancer), Verzenio (breast cancer), and Lenvima (thyroid/endometrial/liver/kidney cancer). These drugs represent over $6 billion in Medicare spending.

Why are Medicare Part D premiums and costs rising despite the price negotiations?

The negotiations offer savings on specific high-cost drugs, but the broader Part D benefit redesign including a $2,100 out-of-pocket cap and the elimination of catastrophic coinsurance has shifted significant costs to insurance plans. This led to a 35% surge in insurer bids for 2026.

Are there any exemptions for oncology drugs under the IRA?

Yes. Drugs with a single orphan designation for a single disease are exempt from negotiation. However, most oncology drugs seek multiple indications over their lifecycle, which would disqualify them from this exemption.

References

Impact of Medicare Price “Negotiation” Program on small and large molecule medicines - Charles River Associates

How CBO Estimated the Budgetary Impact of Key Prescription Drug Provisions in the 2022 Reconciliation Act

Stakeholders Hope Bill Will Create IRA Drug Negotiation Parity Between Biologics and Small Molecules - Don Davis

Win the Patent Cliff: How the 12-Year Biologic Advantage Reshapes the Drug Market

Drugs likely subject to Medicare negotiation, 2026-2028 - PMC - NIH

Study Finds Postapproval Cancer Trials Fell After Inflation Reduction Act - The ASCO Post

Biotechnology Pharmaceutical Industry: Data Reports 2026 - WifiTalents

Key Facts About Medicare Drug Price Negotiation | KFF

Drug Pricing Reform Proposals: Considerations for Cancer Care

Medicare Drug Price Negotiation Program: Selected Drugs ... - CMS

Key Facts About Medicare Drug Price Negotiation - KFF

Fyreignis Market Research | Reports & Strategy for Rare Diseases ...

Effect of the Inflation Reduction Act on Drug Innovation - ISPOR

The Inflation Reduction Act Is Negotiating the United States Out of Drug Innovation

The Inflation Reduction Act and Drug Development: Potential Early ...

New FDA guidance could elevate pharma's biosimilar market | BioPharma Dive

Novel Drug Approvals for 2026 | FDA

FDA Approvals in Oncology: January-March 2026 | Blog | AACR

Models attempting to quantify the relationship between drug development and financial return are missing a key element: the effect on post-approval research - PMC

Early impact of the Inflation Reduction Act on small molecule vs biologic post-approval oncology trials - PubMed

A Call for New Research in the Area of Spending on Medicare Part D | Congressional Budget Office

Medicare and You Handbook 2026

A Current Snapshot of the Medicare Part D Prescription Drug Benefit - KFF

The Budget-Busting Inflation Reduction Act | Cato at Liberty Blog

How much does Medicare drug coverage cost?

Oncology Drug Report 2026

The Biosimilar Paradox: 2026 Market Report on Systemic Challenges, Policy Collisions, and the Future of Biologic Competition - DrugPatentWatch

The Pharmaceutical Industry in 2025: An Analysis of FDA Drug Approvals from the Perspective of Molecules - PMC

Explaining the Prescription Drug Provisions in the Inflation Reduction Act - KFF

BIOSIMILARS REPORT - Cardinal Health

The biggest FDA decision drops in 2026 so far: Oncology approvals | MDLinx

Oncology (Cancer)/Hematologic Malignancies Approval Notifications - FDA

Cancer Policy Monitor: February 10, 2026

What Recent Federal Law Changes Impact the Cancer Community?

Proposed NIH Cuts, Funding Changes Risk Slowing Cancer Research - ASCO

VIA ELECTRONIC FILING TO: www.regulations.gov February 23, 2026 The Honorable Mehmet Oz, MD Administrator Centers for Medicare & - Biotechnology Innovation Organization | BIO

Global Benchmark for Efficient Drug Pricing (GLOBE) Model - Federal Register

Lessons From Europe's Loss of Biopharma Leadership, and Its Attempts to Recover

Navigation

© 2026 FyreIgnis Market Research. All rights reserved.

Legal

info@fyreignismarketresearch.com

India