The Orphan Drug Paradox

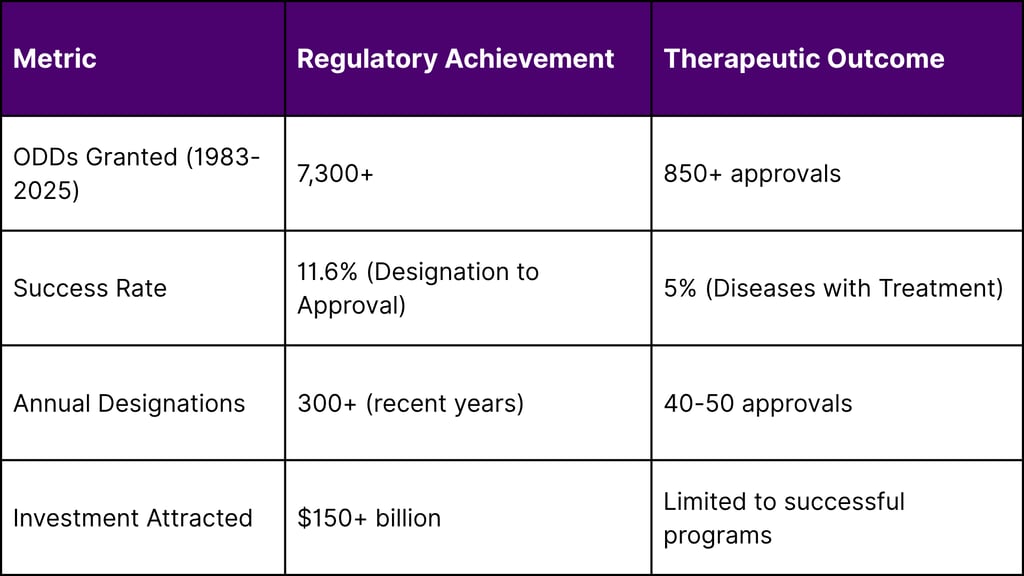

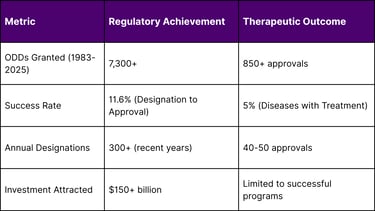

The pharmaceutical industry faces a profound paradox: while the FDA has granted over 7,300 Orphan Drug Designations (ODDs) since 1983, only 5% of the estimated 7,000+ rare diseases have approved treatments. This disconnect between regulatory support and therapeutic availability reveals systemic challenges in rare disease drug development, creating both a humanitarian crisis and a massive commercial opportunity. This comprehensive analysis examines the root causes of this paradox, quantifies the market gaps, and identifies strategic solutions for bridging the treatment divide.

The Magnitude of the Problem

The Numbers Behind the Paradox

The stark reality of rare disease treatment availability:

Total Rare Diseases: 7,000+ identified conditions

FDA Orphan Drug Designations: 7,300+ granted since 1983

Diseases with Approved Treatments: ~350 (5% of total)

Patients Affected: 400+ million globally

Market Opportunity: $374+ billion by 2030

Regulatory Success vs. Therapeutic Reality

Understanding Orphan Drug Designation

The FDA Framework

The Orphan Drug Act of 1983 established criteria for ODD:

Prevalence Threshold: <200,000 patients in the U.S.

Regulatory Incentives: 7-year market exclusivity

Financial Benefits: 50% tax credit for clinical costs

Development Support: FDA guidance and fee waivers

EMA Orphan Medicine Designation

The European framework provides additional support:

Prevalence Threshold: <5 in 10,000 people

Market Exclusivity: 10 years

Protocol Assistance: Reduced-fee scientific advice

Centralized Procedure: EU-wide approval pathway

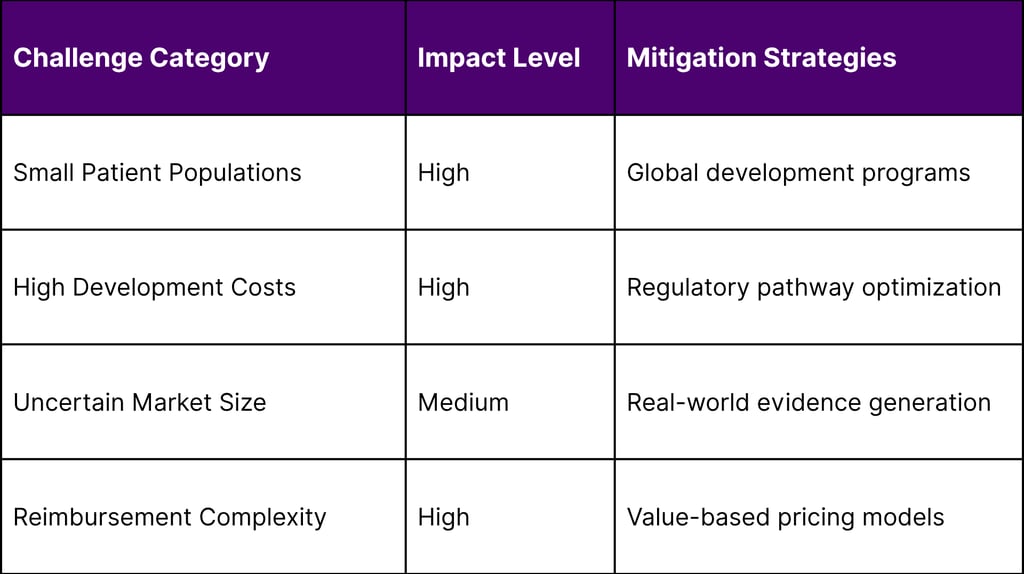

The Development Challenge Matrix

Scientific Complexity Barriers

Disease Heterogeneity:

Multiple genetic variants within single diseases

Phenotypic variability across patients

Limited understanding of disease mechanisms

Lack of validated biomarkers

Research Infrastructure Gaps:

Insufficient patient registries

Limited natural history data

Inadequate diagnostic tools

Scarce clinical trial sites

Commercial Viability Challenges

Development Timeline Analysis

Typical Rare Disease Development:

Discovery to IND: 5-7 years

Clinical Development: 8-12 years

Regulatory Review: 1-2 years

Total Timeline: 14-21 years

Total Investment: $500M-$2.5B

Disease Category Analysis

Neurological Disorders: Highest Unmet Need

Disease Burden:

Total Neurological Rare Diseases: 1,200+

Diseases with Treatments: 45 (3.8%)

Patient Population: 12+ million globally

Treatment Gap: 96.2%

Key Examples:

Huntington's Disease: ODD granted 1990, first approval 2017

ALS: Multiple ODDs, limited treatment options

Rare Epilepsies: Hundreds of conditions, <20 treatments

Neuromuscular Disorders: Significant progress but vast gaps remain

Metabolic Disorders: Moderate Success

Disease Burden:

Total Metabolic Rare Diseases: 800+

Diseases with Treatments: 85 (10.6%)

Patient Population: 8+ million globally

Treatment Gap: 89.4%

Success Factors:

Well-characterized biochemical pathways

Established diagnostic methods

Enzyme replacement therapy platforms

Academic research infrastructure

Oncological Rare Diseases: Emerging Focus

Disease Burden:

Total Rare Cancers: 200+

Diseases with Treatments: 45 (22.5%)

Patient Population: 6+ million globally

Treatment Gap: 77.5%

Development Advantages:

Established oncology infrastructure

Regulatory pathway familiarity

Biomarker development expertise

Investment community comfort

Regional Development Patterns

United States: Regulatory Leadership

Development Characteristics:

ODDs Granted: 7,300+ (global leader)

Approval Success Rate: 11.6%

Average Development Time: 12-15 years

Investment Concentration: 60% of global funding

Enabling Factors:

Robust regulatory framework

Strong intellectual property protection

Advanced clinical research infrastructure

Venture capital ecosystem

European Union: Harmonized Approach

Development Characteristics:

Orphan Designations: 2,500+ since 2000

Approval Success Rate: 14.2%

Cross-Border Collaboration: Enhanced efficiency

Academic Excellence: Strong research base

Asia-Pacific: Emerging Hub

Development Characteristics:

Regulatory Evolution: Rapid framework development

Manufacturing Advantages: Cost-effective production

Population Genetics: Unique disease patterns

Government Support: Increasing investment

The Economics of Rare Disease Development

Cost Structure Analysis

Development Cost Breakdown:

Preclinical Research: $50-100M (25-30%)

Clinical Trials: $150-300M (45-50%)

Regulatory Affairs: $25-50M (8-10%)

Manufacturing Setup: $75-150M (15-20%)

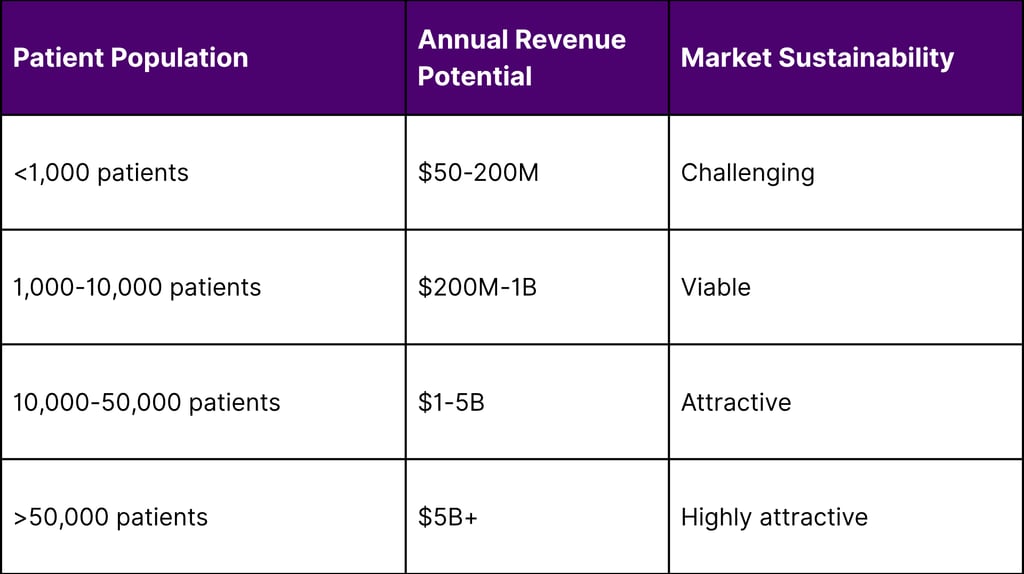

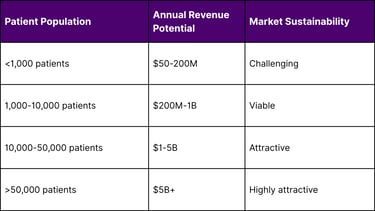

Revenue Potential Assessment

Return on Investment Analysis

Successful Rare Disease Programs:

Peak Sales: $2-8B annually

Development ROI: 15-25%

Time to Peak Sales: 8-12 years post-approval

Market Exclusivity: 7-10 years

Technology Solutions Addressing the Gap

Platform Approaches

Gene Therapy Platforms:

Adeno-Associated Virus (AAV): Broad applicability

Lentiviral Vectors: Stable gene expression

CRISPR/Cas9: Precise gene editing

Base Editing: Reduced off-target effects

Drug Repurposing Strategies:

AI-Driven Discovery: Accelerated identification

Phenotypic Screening: Mechanism-agnostic approaches

Combination Therapies: Enhanced efficacy

Regulatory Pathways: Faster approval routes

Manufacturing Innovation

Flexible Manufacturing:

Modular Systems: Scalable production

Quality by Design: Built-in compliance

Continuous Manufacturing: Reduced costs

Distributed Networks: Regional production

Investment Landscape Evolution

Venture Capital Trends

Funding Patterns (2020-2025):

Total Investment: $45B in rare disease companies

Average Series A: $40M

Late-Stage Rounds: $150M average

Exit Values: $5-15B for successful programs

Strategic Partnership Models

Risk-Sharing Approaches:

Pharma-Biotech Partnerships: Shared development costs

Government Collaborations: Public-private partnerships

Patient Foundation Funding: Community-driven support

International Consortiums: Global development programs

Regulatory Innovation Addressing the Gap

FDA Modernization Initiatives

Accelerated Pathways:

Breakthrough Therapy Designation: Expedited review

Accelerated Approval: Surrogate endpoints

Fast Track Designation: Rolling submissions

Priority Review: Shortened timelines

Guidance Development:

Complex Innovative Trial Designs: Adaptive approaches

Real-World Evidence: Post-market requirements

Patient-Focused Drug Development: Stakeholder engagement

Rare Disease Endpoints: Fit-for-purpose measures

International Harmonization

Regulatory Convergence:

ICH Guidelines: Standardized requirements

Joint Scientific Advice: Coordinated guidance

Mutual Recognition: Reduced duplication

Global Development Programs: Synchronized timelines

Patient Advocacy and Disease Awareness

Foundation Impact

Patient Organization Contributions:

Disease Registries: Natural history data

Research Funding: $2B+ annually

Regulatory Advocacy: Policy influence

Patient Engagement: Clinical trial participation

Digital Health Solutions

Technology Enablers:

Telemedicine: Expanded access

Wearable Devices: Continuous monitoring

Digital Biomarkers: Objective measures

Patient-Reported Outcomes: Quality of life metrics

Market Access Innovation

Value-Based Pricing Models

Innovative Approaches:

Outcomes-Based Contracts: Performance guarantees

Indication-Specific Pricing: Targeted value

Installment Payments: Budget management

Risk-Sharing Agreements: Shared uncertainty

Global Access Programs

Expanding Availability:

Named Patient Programs: Pre-approval access

Compassionate Use: Emergency access

International Pricing: Tiered structures

Donation Programs: Humanitarian access

Strategic Solutions to Bridge the Gap

For Pharmaceutical Companies

Portfolio Strategy:

Platform Investments: Versatile technology platforms

Partnership Models: Risk-sharing collaborations

Regulatory Excellence: Accelerated pathway expertise

Global Development: Coordinated international programs

Operational Excellence:

Adaptive Trial Designs: Flexible development approaches

Real-World Evidence: Post-market data generation

Patient Engagement: Community partnership

Manufacturing Flexibility: Scalable production systems

For Biotech Companies

Development Focus:

Mechanism Innovation: Novel therapeutic approaches

Biomarker Development: Precision medicine applications

Combination Strategies: Enhanced efficacy

Regulatory Strategy: Optimal pathway selection

Commercial Preparation:

Market Access Planning: Early payer engagement

Patient Support Programs: Comprehensive services

Global Expansion: International partnerships

Digital Health Integration: Technology-enabled care

For Investors

Investment Strategies:

Portfolio Diversification: Balanced risk distribution

Platform Technologies: Broad applicability

Regulatory Expertise: Development success factors

Global Opportunities: International expansion potential

Risk Management:

Clinical Development Risks: Milestone-based funding

Regulatory Pathway Risks: Multiple strategy approaches

Commercial Risks: Market access preparation

Technology Risks: Platform diversification

Emerging Solutions and Future Outlook

Artificial Intelligence Applications

AI-Driven Solutions:

Drug Discovery: Accelerated target identification

Patient Stratification: Precision medicine approaches

Clinical Trial Design: Optimized protocols

Regulatory Strategy: Pathway optimization

Gene and Cell Therapy Revolution

Therapeutic Platforms:

In Vivo Gene Editing: Direct therapeutic application

Cell Reprogramming: Regenerative approaches

Synthetic Biology: Engineered therapeutic systems

Tissue Engineering: Replacement strategies

Regulatory Evolution

Future Frameworks:

Adaptive Licensing: Flexible approval processes

Real-World Evidence Integration: Post-market surveillance

Patient-Centric Endpoints: Meaningful measures

Global Harmonization: Coordinated requirements

Quantifying the Opportunity

Market Sizing Analysis

Total Addressable Market (2030):

Treated Diseases (5%): $150B

Untreated Diseases (95%): $2.85T potential

Realistic Capture (20% by 2030): $570B opportunity

Investment Required: $200-300B

Development Pipeline Analysis

Current Pipeline Strength:

Preclinical Programs: 2,500+ active

Phase I/II Trials: 800+ ongoing

Phase III Trials: 150+ active

Regulatory Submissions: 50+ expected annually

Conclusion

The orphan drug paradox represents both the greatest challenge and the most significant opportunity in pharmaceutical development today. While the gap between regulatory support and therapeutic availability is stark—with only 5% of rare diseases having approved treatments despite 7,300+ FDA designations—this disconnect illuminates a path forward for industry transformation.

The root causes of this paradox are complex and interconnected: scientific challenges, commercial constraints, regulatory complexity, and resource limitations. However, emerging solutions across technology platforms, regulatory innovation, and commercial models are beginning to address these fundamental barriers.

The convergence of gene therapy breakthroughs, AI-driven drug discovery, platform technologies, and innovative financing models is creating unprecedented opportunities to bridge the treatment gap. Organizations that can navigate the complex development landscape, build scalable platforms, and create sustainable commercial models will not only serve the humanitarian imperative but also capture significant value in the $374+ billion rare disease market.

The orphan drug paradox is not an insurmountable challenge—it is a call to action for the pharmaceutical industry to innovate, collaborate, and transform. The 400+ million patients affected by rare diseases deserve better than the current 5% treatment availability. The industry has the tools, resources, and regulatory support to dramatically improve these outcomes.

The question is not whether we can solve the orphan drug paradox, but how quickly we can mobilize the resources, partnerships, and innovation necessary to transform this crisis into opportunity. The time for incremental improvement has passed; the moment for revolutionary change is now.

The orphan drug paradox will be remembered as either the greatest missed opportunity in pharmaceutical history or the catalyst that transformed rare disease treatment forever. The choice is ours to make, and the patients are waiting.

FAQs

1. What is the “Orphan Drug Paradox”?

The paradox refers to the disconnect between the 7,300+ FDA Orphan Drug Designations granted since 1983 and the fact that only about 5% of rare diseases currently have an approved treatment. This reveals a major gap between regulatory recognition and therapeutic development.

2. How many rare diseases currently have FDA-approved treatments?

As of 2025, only about 350 out of 7,000+ rare diseases have one or more approved therapies, accounting for just 5% of known rare conditions.

3. Why is there such a low approval rate despite high regulatory activity?

While many drugs receive Orphan Drug Designation (ODD), scientific, commercial, and infrastructure challenges slow down or halt development. The typical approval rate from ODD to actual treatment is around 11.6%.

4. What incentives are offered through the FDA’s Orphan Drug Act?

Approved orphan drugs receive:

7 years of market exclusivity

Tax credits for clinical trial costs

Waived fees for regulatory submissions

Access to FDA guidance throughout development

5. Which rare disease categories face the highest treatment gaps?

Neurological Disorders: Only 3.8% have treatments

Metabolic Disorders: 10.6% treated

Rare Cancers: 22.5% treated

Neurological diseases are the most underserved, despite being among the most debilitating.

6. What are the biggest scientific barriers in rare disease drug development?

Disease heterogeneity

Lack of biomarkers

Small patient populations

Poor understanding of disease mechanisms

These factors complicate both research and clinical trial design.

7. What role does venture capital play in rare disease research?

Venture capital has invested $45B+ between 2020 and 2025, with increasing interest in gene therapy platforms and precision medicine that can scale across multiple rare conditions.

8. Can artificial intelligence (AI) accelerate rare disease drug development?

Yes. AI is being used to:

Identify drug targets faster

Stratify patient populations

Optimize trial designs

Predict regulatory pathways

This speeds up development and lowers costs.

9. Are regulatory agencies adapting to better support orphan drug development?

Yes. The FDA, EMA, and global regulators are implementing:

Accelerated approval pathways

Real-world evidence models

Adaptive trial frameworks

Harmonized international guidance

10. What is the commercial opportunity in solving the orphan drug paradox?

Capturing even 20% of the untreated rare disease space by 2030 could represent a $570B+ market, with long-term exclusivity, premium pricing models, and global patient demand.

11. How can pharmaceutical and biotech companies bridge the treatment gap?

By:

Investing in gene and cell therapy platforms

Building real-world evidence infrastructure

Using adaptive trial designs

Partnering with patient advocacy groups and regulators

Prioritizing scalable, platform-based development

12. What’s the role of patient organizations in rare disease innovation?

They:

Maintain disease registries

Fund early-stage research

Drive trial recruitment

Shape regulatory and policy frameworks

Patient advocacy is critical for momentum and impact.

References

U.S. Food and Drug Administration (FDA) – Orphan Drug Designations and Approvals

European Medicines Agency (EMA) – Orphan Medicines

National Institutes of Health (NIH) – Rare Diseases Research & Support (NCATS)

World Health Organization (WHO) – Global Health Estimates and Rare Disease Impact

Peer-Reviewed Clinical and Policy Research

Navigation

© 2026 FyreIgnis Market Research. All rights reserved.

Legal

info@fyreignismarketresearch.com

India