The Rise of Targeted Alpha Therapies (TAT)

Executive Summary: The Dawn of the Alpha Era in Oncology

The landscape of precision oncology in February 2026 is defined by a fundamental transition in the therapeutic utilization of ionizing radiation. For over a decade, the radiopharmaceutical sector was dominated by beta-emitting isotopes, most notably Lutetium-177 ($^{177}Lu$), which provided a vital proof-of-concept for radioligand therapy (RLT) in neuroendocrine tumors and prostate cancer. However, as the limitations of beta radiation specifically its multi-millimeter range and lower linear energy transfer became clinically evident through the emergence of treatment resistance and off-target toxicities, the industry shifted its focus toward Targeted Alpha Therapy (TAT).

Targeted Alpha Therapy represents a significant technological leap, utilizing heavy, high-energy alpha particles to deliver lethal radiation over a distance of only a few cell diameters. This precision allows for the eradication of micrometastases while sparing adjacent healthy tissue, a feat that traditional radiotherapy and even contemporary beta-emitters often struggle to achieve. The year 2026 stands as the definitive breakout period for this modality, driven by the convergence of three critical factors: the maturation of pivotal Phase 3 clinical data, the stabilization of the previously fragile global isotope supply chain through domestic manufacturing breakthroughs, and an aggressive consolidation phase where Big Pharma has moved from speculative interest to the establishment of "manufacturing moats".

Analysis of the current market suggests that the "Alphabet Era" of oncology is no longer a future prospect but a present reality. With the global radiopharmaceutical market projected to reach $13.4 billion by 2033, the strategic maneuvers observed in early 2026 characterized by record-breaking M&A activity and the scaling of domestic isotope production indicate that TAT is poised to become a first-line treatment for various refractory malignancies.

Radiobiological Foundations: The Physical Imperative for Alpha Emitters

The transition from beta to alpha emitters is not merely a trend but a requirement dictated by the laws of nuclear physics and radiobiology. To understand why 2026 is the breakout year, one must first analyze the physical differences between the two modalities.

Linear Energy Transfer (LET) and DNA Damage

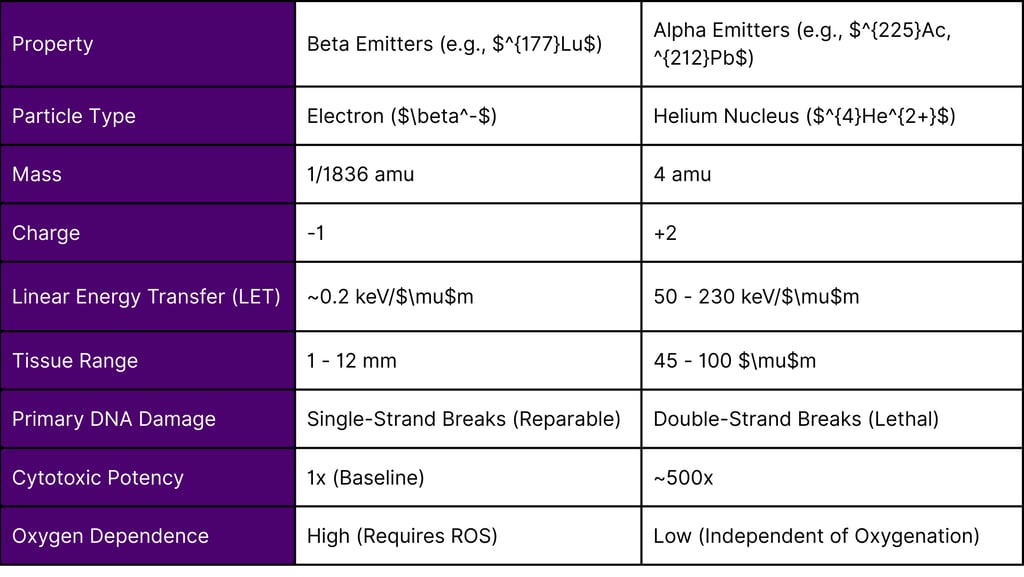

Alpha particles are doubly charged helium-4 nuclei ($^{4}He^{2+}$), possessing a mass approximately 8,000 times greater than the electrons emitted by beta-decaying isotopes. This massive size and charge result in a densely ionizing track structure. In radiobiological terms, alpha emitters exhibit high Linear Energy Transfer (LET), typically ranging from 50 to 230 keV/$\mu$m. In stark contrast, beta particles exhibit a low LET of approximately 0.2 keV/$\mu$m.

The consequence of this difference is found in the nature of DNA damage. Beta radiation primarily causes single-strand breaks (SSBs) in the DNA helix. These breaks are often reparable by cellular enzymes, leading to therapeutic resistance. Alpha radiation, however, induces complex clusters of double-strand breaks (DSBs) that are essentially irreparable. Research indicates that the cytotoxic potency of alpha particles is approximately 500 times greater than that of beta particles, meaning that as few as one to ten alpha-particle traversals of a cell nucleus are sufficient to ensure cell death.

Range and Precision

A critical limitation of beta emitters is their tissue range, which can reach up to 12 mm. While this "cross-fire effect" allows a beta-emitting drug to kill neighboring tumor cells that do not express the target receptor, it also results in significant collateral damage to healthy organs at risk (OARs), such as the bone marrow, salivary glands, and kidneys.

Alpha particles possess a range of only 45 to 100 $\mu$m roughly the diameter of 5 to 10 cells. This ultra-short range ensures that the massive energy payload is deposited almost entirely within the target lesion. This is particularly advantageous for treating micrometastases and disseminated disease, where the tumor burden is small and the risk of healthy tissue irradiation is high.

Table 1: Physical and Biological Properties of Clinical Radiopharmaceutical Payloads

The Strategic Shift: Why Big Pharma is on an Acquisition Spree

The period between 2024 and 2026 has been marked by a frenzy of M&A activity, with large-cap pharmaceutical companies spending tens of billions of dollars to acquire radiopharmaceutical platforms. The rationale for this "acquisition spree" is multifaceted, extending beyond simple pipeline expansion into the territory of strategic "reinvention".

The Patent Cliff and the Search for Differentiated Assets

As traditional small molecules and biologics face increasing pricing pressure from the Inflation Reduction Act (IRA) and looming patent expirations, Big Pharma is desperately seeking high-barrier-to-entry therapeutic areas. Radiopharmaceuticals, particularly TAT, offer a unique "moat" because they require specialized regulatory licenses, nuclear manufacturing capabilities, and complex "just-in-time" logistics that traditional generics manufacturers cannot easily replicate.

Building the "Manufacturing Moat"

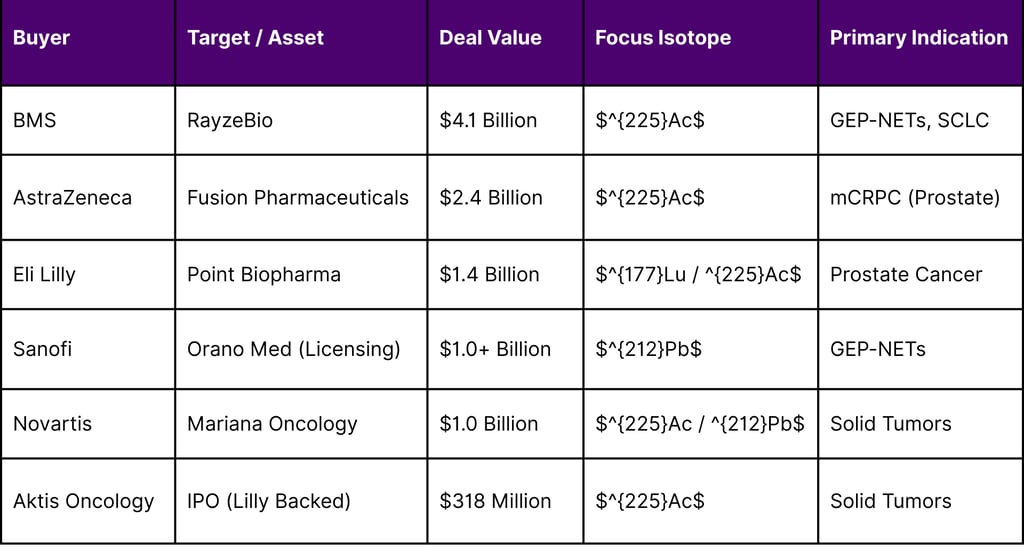

A standout trend in 2026 is the shift from acquiring intellectual property (IP) to acquiring infrastructure. In more than 80% of radiopharma deals analyzed in 2025, the integration of manufacturing or isotope supply was a primary driver. Because isotopes like Actinium-225 ($^{225}Ac$) have half-lives of less than ten days, the ability to manufacture the drug close to the patient is a critical competitive advantage.

Bristol Myers Squibb (BMS): The $4.1 billion acquisition of RayzeBio in early 2024 was not just for the lead asset RYZ101 but also for RayzeBio’s state-of-the-art 63,000-square-foot manufacturing facility in Indianapolis.

AstraZeneca: The $2.4 billion deal for Fusion Pharmaceuticals provided AstraZeneca with a fully operational, GMP-compliant radiopharmaceutical manufacturing facility, ensuring they could bypass the logistical bottlenecks that often stall smaller biotechs.

Eli Lilly: By acquiring Point Biopharma for $1.4 billion, Lilly gained access to a 77,000-square-foot manufacturing hub, which they have since bolstered with a $6 billion investment in active pharmaceutical ingredient (API) facilities.

Table 2: Major Radiopharmaceutical M&A Transactions (2024 - 2026)

2026: The Clinical Breakout and Key Trial Readouts

The transition of TAT from an experimental modality to a clinical standard is reaching a tipping point in February 2026, as several high-stakes trials report their findings. These trials are essential for demonstrating that alpha emitters can succeed where beta emitters fail specifically in patients who have progressed after $^{177}Lu$ therapy.

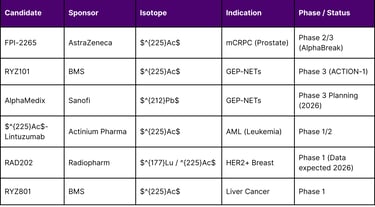

The AlphaBreak Trial (Fusion Pharmaceuticals)

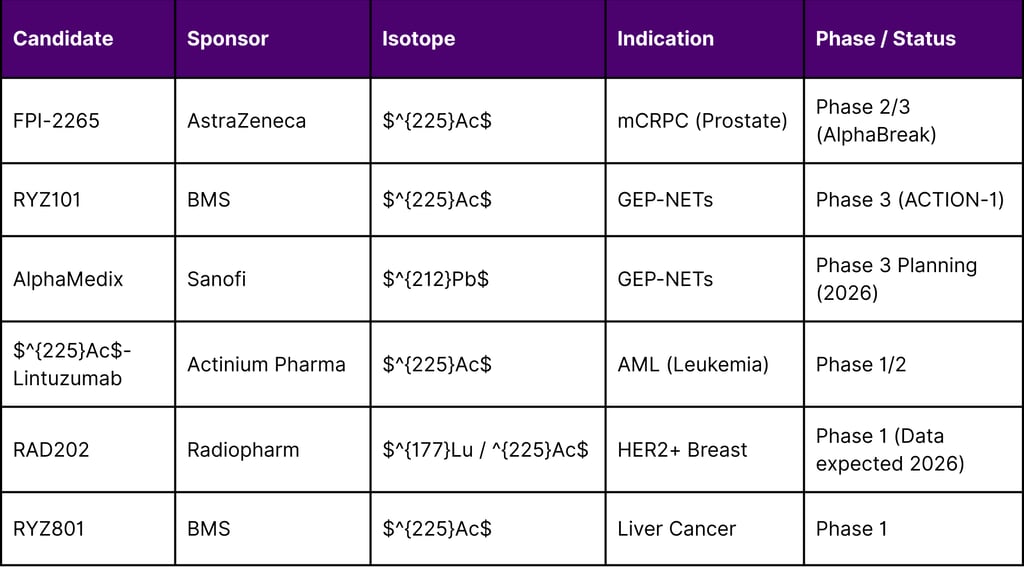

The Phase 2/3 AlphaBreak trial (NCT06402331) is currently the most watched study in the prostate cancer space. Evaluating FPI-2265 ($^{225}Ac$-PSMA-I&T), the trial targets metastatic castration-resistant prostate cancer (mCRPC) in patients previously treated with $^{177}Lu$-PSMA radioligand therapy. Interim data from the preceding TATCIST study showed that $^{225}Ac$ could induce significant PSA declines in patients who were otherwise refractory to beta radiation, paving the way for the global registrational Phase 3 portion that is a cornerstone of AstraZeneca's 2026 strategy.

The ACTION-1 Trial (RayzeBio/BMS)

RayzeBio’s ACTION-1 (NCT05477576) is a Phase 1b/3 study of RYZ101 ($^{225}Ac$-DOTAMTATE) in patients with somatostatin receptor-positive (SSTR+) gastroenteropancreatic neuroendocrine tumors (GEP-NETs). The study is groundbreaking for including a first-of-its-kind dosimetry sub-study, which utilized SPECT/CT to image alpha-emitting daughter products ($^{221}Fr$ and $^{213}Bi$). This research proved that the alpha-emitting payload remains localized within the tumor, providing the rigorous safety and efficacy data required for regulatory approval in 2026.

AlphaMedix and the Lead-212 Revolution (Sanofi/Orano Med)

In late 2025, data from the ALPHAMEDIX-02 Phase 2 study demonstrated an impressive 60% overall response rate (ORR) in RLT-naive patients with GEP-NETs and a 34.6% ORR in patients who had previously failed $^{177}Lu$ therapy. Lead-212 ($^{212}Pb$) acts as an in situ generator of alpha particles, and its shorter half-life (10.6 hours) offers significant translational advantages in terms of patient throughput and radiation protection compared to the longer-lived $^{225}Ac$.

Table 3: Status of Lead Targeted Alpha Therapy Candidates (February 2026)

Overcoming the "Isotope Wars": Supply Chain Evolution in 2026

The greatest hurdle for radiopharmaceuticals has historically been the scarcity of the radioactive "fuel." Before 2025, the world relied on aging nuclear reactors in Russia and Europe for isotopes like $^{225}Ac$. However, 2026 marks the first year of a stabilized, "on-shored" supply chain.

The DOE Isotope Program (DOE IP)

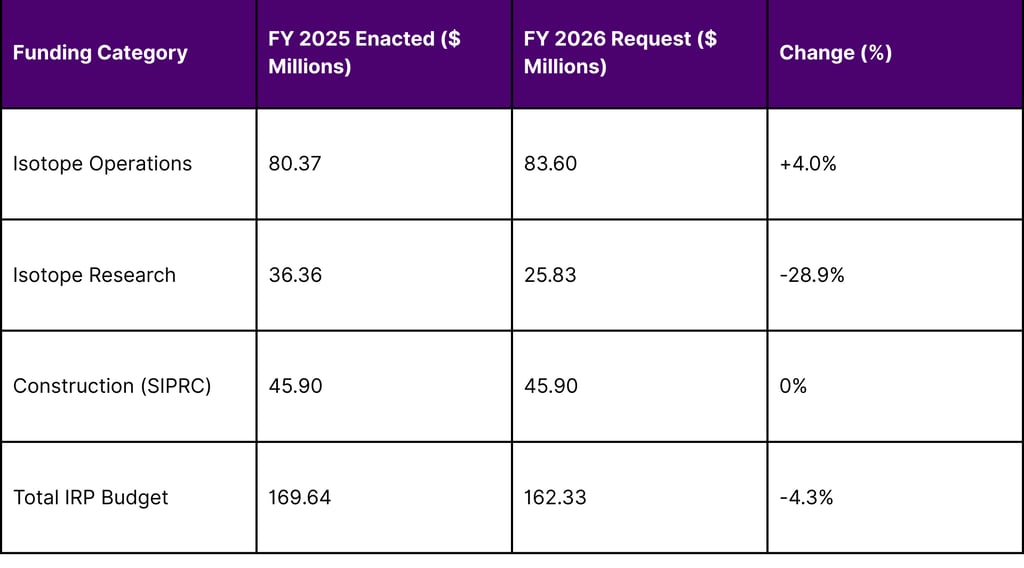

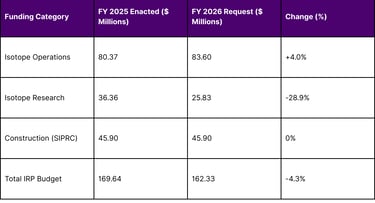

The U.S. Department of Energy (DOE) has significantly ramped up its domestic production capabilities. The FY 2026 budget request for Isotope R&D and Production stands at $162.3 million, focusing on ensuring "American isotope independence". Key projects reaching maturity in 2026 include the Stable Isotope Production and Research Center (SIPRC) and the refurbishment of cyclotrons at Brookhaven National Laboratory specifically for $^{225}Ac$ production.

The Rise of Private Producers: Nusano’s Utah Facility

Perhaps the most significant development for the 2026 breakout was the ribbon-cutting of Nusano’s 190,000-square-foot facility in West Valley City, Utah, in August 2025. This facility uses a patented ion source to produce high-volume radioisotopes, including $^{225}Ac$, $^{211}At$, and $^{67}Cu$. By February 2026, Nusano has entered into long-term supply agreements with major developers like AstraZeneca and Ratio Therapeutics, effectively ending the period of "isotope rationing" that had stifled clinical trials for years.

Table 4: DOE Isotope Program Financial Summary (FY 2025-2026)

The Socioeconomic Burden: Epidemiology and Unmet Needs in 2026

The commercial necessity for TAT is driven by a massive, growing patient population with few remaining options. As of February 2026, cancer remains a leading cause of death globally, with projections indicating an increasing incidence rate in the United States.

2026 Projections and the Role of Targeted Therapy

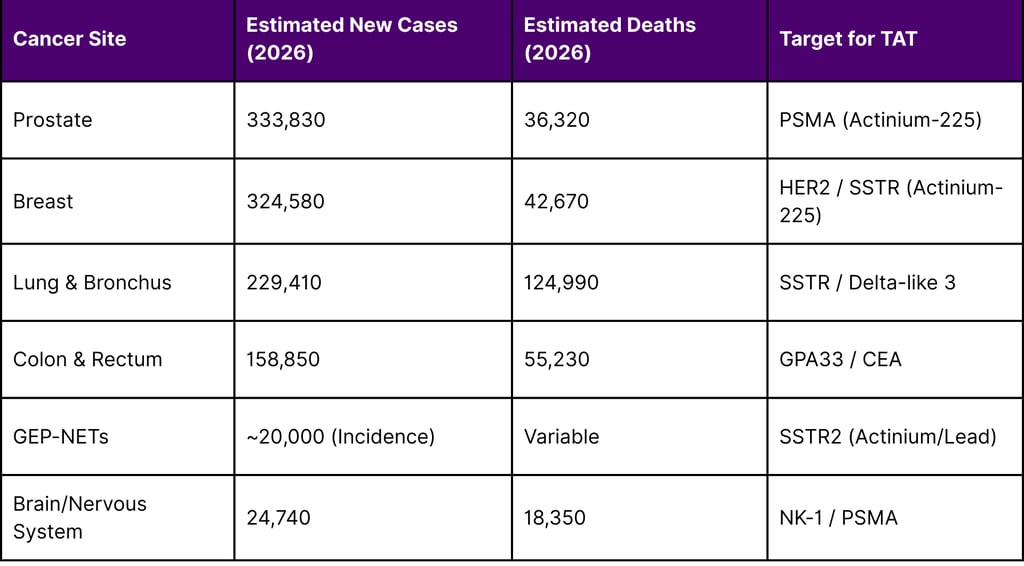

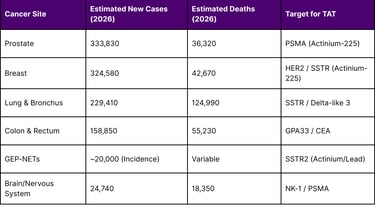

Approximately 2,114,850 new cancer cases are expected to be diagnosed in the U.S. in 2026, with over 626,000 deaths. Prostate cancer remains the leading site of new cases in men (333,830 projected for 2026), and breast cancer in women (321,910 projected).

Radioligand therapy has already established a role in prostate cancer through $^{177}Lu$-PSMA-617 (Pluvicto). However, data suggests that many patients eventually progress on beta therapy or have "PSMA-low" expression that beta particles cannot effectively treat. This creates a massive market for alpha-emitters, which can overcome these resistance mechanisms. Furthermore, the application of TAT is expanding into rare but lethal tumors, such as extensive-stage small cell lung cancer (ES-SCLC) and glioblastoma, where five-year survival rates remain abysmal.

Table 5: Projected New Cancer Cases and Deaths in the US (2026)

The Economic Outlook: 2025/2026 Financial Results and Forecasts

February 2026 is also a pivotal month for financial reporting, with Big Pharma leaders providing guidance on their radiopharmaceutical investments.

AstraZeneca (Feb 10, 2026): Reported a strong 2025 with $58.7 billion in total revenue and 16 blockbuster medicines. CEO Pascal Soriot highlighted the "transformative technologies" in their pipeline, including their growing radiopharmaceutical portfolio, as key drivers for their $80 billion sales goal by 2030.

Eli Lilly (Feb 4, 2026): Issued a robust 2026 revenue guidance of $80 billion to $83 billion. Despite a $484 million impairment charge in 2025 related to assets from the Point Biopharma acquisition, Lilly confirmed continued investment in its radioligand platform as a core pillar of its "Innovation Economy" strategy.

The IPO Market: The January 2026 IPO of Aktis Oncology, which raised $318 million with backing from Eli Lilly, signals that public markets are once again hungry for differentiated radiopharmaceutical platforms.

Conclusion: A Turning Point in Human Health

As the data from early 2026 confirms, Targeted Alpha Therapy is no longer a niche research interest; it is a clinical and commercial imperative. The shift from beta to alpha emitters is driven by a superior biological mechanism of action that addresses the most difficult challenges in oncology hypoxia, micrometastatic spread, and therapeutic resistance.

With a stabilized supply chain, multibillion-dollar investments from the world's largest pharmaceutical companies, and pivotal Phase 3 data on the horizon, 2026 is the year the "Alphabet Era" becomes the new standard of care. For the oncology community and the millions of patients facing refractory disease, TAT offers a level of precision and potency that was previously unimaginable.

Frequently Asked Questions (FAQ)

1. What makes Targeted Alpha Therapy (TAT) better than traditional radiation?

Traditional radiation (external beam) and beta-emitting drugs often have a range that causes damage to healthy surrounding tissue. TAT uses alpha particles that have a very short range (only 5-10 cell diameters) and a much higher energy level. This allows the radiation to kill cancer cells with high precision while sparing healthy organs.

2. Why is Big Pharma so interested in this space in 2026?

Big Pharma is facing "patent cliffs" for their older drugs and is looking for specialized, high-margin fields. Radiopharmaceuticals are difficult to manufacture and distribute, creating a natural competitive "moat." Companies like BMS, AstraZeneca, and Lilly are acquiring these platforms to control the entire supply chain, from isotope production to final delivery.

3. Is Actinium-225 the only isotope used in TAT?

No, while Actinium-225 ($^{225}Ac$) is the most widely studied, other isotopes like Lead-212 ($^{212}Pb$) and Astatine-211 ($^{211}At$) are showing significant promise. Lead-212 is particularly notable for its shorter half-life and translational advantages in neuroendocrine tumors.

4. How is the supply of these isotopes managed in 2026?

The supply chain has stabilized thanks to two major shifts: increased funding for the U.S. Department of Energy (DOE) Isotope Program and the entry of private companies like Nusano, which opened a massive production facility in Utah in late 2025.

5. Can TAT treat cancers that are resistant to other therapies?

Yes. Because alpha particles kill cells via direct physical destruction of DNA (double-strand breaks) rather than through chemical reactions that require oxygen, they are effective against hypoxic (oxygen-starved) tumors and cancers that have stopped responding to beta radiation or chemotherapy.

6. What are the main challenges for TAT in 2026?

The main challenges remain the high cost of production, the need for specialized "just-in-time" logistics due to the short half-life of isotopes, and the requirement for highly specialized medical staff and facilities to handle radioactive materials.

References

AstraZeneca. (2026, February 10). Full Year and Q4 2025 results announcement.

Bain & Company. (2026, January 27). M&A in Pharmaceuticals: Bigger, Bolder, and Far More Strategic.

Bristol Myers Squibb. (2026, February 5). Form 8-K: Current report filing.

Department of Energy (DOE). (2025, March). FY 2026 Isotope R&D and Production Budget Request to Congress.

Eli Lilly and Company. (2026, February 4). Lilly reports fourth-quarter 2025 financial results and provides 2026 guidance.

National Cancer Institute (NCI). (2026). SEER Cancer Stat Facts: Cancer Projections 2026.

Nusano, Inc. (2025, August 21). Nusano cuts ribbon on state-of-the-art radioisotope production facility in Utah.

Sanofi. (2025, October 20). ESMO: AlphaMedix phase 2 data support first-in-class potential of new targeted alpha therapy.

U.S. Food and Drug Administration (FDA). (2025). Novel Drug Approvals for 2025.

Navigation

© 2026 FyreIgnis Market Research. All rights reserved.

Legal

info@fyreignismarketresearch.com

India